Here are some of the key tax-related deadlines affecting businesses and other employers during the first quarter of 2023. Keep in mind that this list isn’t all-inclusive, so there may be additional deadlines that apply to you. If you have questions about filing requirements, contact us. We can ensure you’re meeting all applicable deadlines.

Give annual information statements to recipients of certain payments you made during 2022. You can use the appropriate version of Form 1099 or other information return. Form 1099 can be issued electronically with the consent of the recipient. This due date applies only to the following types of payments:

© 2022

If you own a business, you may wonder if you’re eligible to take the qualified business income (QBI) deduction. Sometimes this is referred to as the pass-through deduction or the Section 199A deduction.

The QBI deduction is:

Taxpayers other than corporations may be entitled to a deduction of up to 20% of their QBI. For 2022, if taxable income exceeds $170,050 for single taxpayers, or $340,100 for a married couple filing jointly, the QBI deduction may be limited based on different scenarios. For 2023, these amounts are $182,100 and $364,200, respectively.

The situations in which the QBI deduction may be limited include whether the taxpayer is engaged in a service-type of trade or business (such as law, accounting, health or consulting), the amount of W-2 wages paid by the trade or business, and/or the unadjusted basis of qualified property (such as machinery and equipment) held by the trade or business. The limitations are phased in.

Some taxpayers may be able to achieve significant savings with respect to this deduction (or be subject to a smaller phaseout of the deduction), by deferring income or accelerating deductions at year-end so that they come under the dollar thresholds for 2022. Depending on your business model, you also may be able to increase the deduction by increasing W-2 wages before year-end. The rules are quite complex, so contact us with questions and consult with us before taking the next steps.

© 2022

The Silent Generation and Baby Boomers are incredibly fortunate generations—and so might be their heirs. Cerulli’s U.S. High-Net-Worth and Ultra-High-Net-Worth Markets 2021 report predicts these generations will transfer $72.6 trillion in assets to heirs and $11.9 trillion to charities through 2045.

That’s a lot of money, and it presents a unique opportunity for Gen Xers and Millennials to secure their financial futures. But it’s important to remember that this wealth won’t just magically appear. It will take planning and communication between the generations to transfer it smoothly.

Managing expectations is one of the biggest challenges heirs face when inheriting wealth from their parents or grandparents. Many Gen Xers and Millennials believe they will inherit a large sum of money, but this may not be the case.

Older generations are living longer and may spend a large percentage of their estate before it can be passed on. Others might give away too much money now and need financial support from their adult children later.

The first step in any estate planning discussion is getting honest about what heirs hope to receive and what the older generation can afford to give.

Older generations can find it difficult to talk about their death. They may feel like they are losing control over their life and finances. Or they may be afraid that their heirs won’t be able to handle the responsibility of inheriting wealth.

However, it’s essential for members of different generations to have open communication about estate planning. That way, everyone is on the same page when the time comes to hand over the reins.

Involving a third party—a CPA, financial advisor, or attorney—in these conversations can help. These professionals do more than ensure the estate planning documents are in order and help navigate tax issues. They can also help facilitate difficult conversations between family members and negotiate any conflicts that might arise during the process. By working with these professionals, families can avoid costly legal disputes and ensure that their wealth is transferred seamlessly from one generation to the next.

Even if the younger generation has a good idea of how much they’ll inherit, there may be some surprises. For example, they may inherit assets that must be managed carefully, such as a business or real estate. Or they may be expected to take over their parent or grandparents’ philanthropic activities.

Members of the younger generation who were kept in the dark about these decisions often struggle to live up to expectations.

If you plan on leaving a legacy for your heirs, start educating them about your intentions. Make sure they understand the role you expect them to play in managing and using the wealth you leave behind.

Every estate plan is unique, but with a long runway and proper planning, most estate tax is avoidable. The key is to start right away—as soon as it’s clear that are assets you want to transfer.

Some simple strategies you can start implementing now include:

When transferring wealth from one generation to the next, specific strategies will vary depending on whether you own a business, have philanthropic inclinations, and who your heirs are. However, what doesn’t change from one estate plan to the next is the need for communication.

For any generational wealth transfer to be successful, heirs need to understand why the wealth is being transferred, how it will be managed, and their role in the process.

Failure to communicate effectively can lead to many problems, including family feuds and lost money. So, families need to have open discussions about generational wealth transfer early on—before any decisions are made. Managing expectations and having honest conversations can help your family avoid misunderstandings and ensure the transition goes as smoothly as possible.

These days, most businesses have some intangible assets. The tax treatment of these assets can be complex.

IRS regulations require the capitalization of costs to:

Capitalized costs can’t be deducted in the year paid or incurred. If they’re deductible at all, they must be ratably deducted over the life of the asset (or, for some assets, over periods specified by the tax code or under regulations). However, capitalization generally isn’t required for costs not exceeding $5,000 and for amounts paid to create or facilitate the creation of any right or benefit that doesn’t extend beyond the earlier of 1) 12 months after the first date on which the taxpayer realizes the right or benefit or 2) the end of the tax year following the tax year in which the payment is made.

The term “intangibles” covers many items. It may not always be simple to determine whether an intangible asset or benefit has been acquired or created. Intangibles include debt instruments, prepaid expenses, non-functional currencies, financial derivatives (including, but not limited to options, forward or futures contracts, and foreign currency contracts), leases, licenses, memberships, patents, copyrights, franchises, trademarks, trade names, goodwill, annuity contracts, insurance contracts, endowment contracts, customer lists, ownership interests in any business entity (for example, corporations, partnerships, LLCs, trusts, and estates) and other rights, assets, instruments and agreements.

Here are just a few examples of expenses to acquire or create intangibles that are subject to the capitalization rules:

The IRS regulations generally characterize an amount as paid to “facilitate” the acquisition or creation of an intangible if it is paid in the process of investigating or pursuing a transaction. The facilitation rules can affect any type of business, and many ordinary business transactions. Examples of costs that facilitate acquisition or creation of an intangible include payments to:

Like most tax rules, these capitalization rules have exceptions. There are also certain elections taxpayers can make to capitalize items that aren’t ordinarily required to be capitalized. The above examples aren’t all-inclusive, and given the length and complexity of the regulations, any transaction involving intangibles and related costs should be analyzed to determine the tax implications.

Contact us to discuss the capitalization rules to see if any costs you’ve paid or incurred must be capitalized or whether your business has entered into transactions that may trigger these rules. You can also contact us if you have any questions.

© 2022

If you have money invested in the stock market, you’re well aware of potential volatility. Needless to say, this volatility can affect your net worth, thus affecting your lifestyle. Something you might not think about is the potential effect on your estate tax liability. Specifically, if the value of stocks or other assets drops precipitously soon after your death, estate tax could be owed on value that has disappeared. One strategy to ease estate tax liability in this situation is for the estate’s executor to elect to use an alternate valuation date.

Typically, assets owned by the deceased are included in his or her taxable estate based on their value on the date of death. For instance, if an individual owned stocks valued at $1 million on the day when he or she died, the stocks would be included in the estate at a value of $1 million.

Despite today’s favorable rules that allow a federal gift and estate tax exemption of $12.06 million, a small percentage of families still must contend with the federal estate tax. However, the tax law provides some relief to estates that are negatively affected by fluctuating market conditions. Instead of using the value of assets on the date of death for estate tax purposes, the executor may elect an “alternate valuation” date of six months after the date of death. This election could effectively lower a federal estate tax bill.

The election is permissible only if the total value of the gross estate is lower on the alternate valuation date than it was on the date of death. Of course, the election generally wouldn’t be made otherwise. If assets are sold after death, the date of the disposition controls. The value doesn’t automatically revert to the date of death.

Furthermore, the ensuing estate tax must be lower by using the alternate valuation date than it would have been using the date-of-death valuation. This would also seem to be obvious, but that’s not necessarily true for estates passing under the unlimited marital deduction or for other times when the estate tax equals zero on the date of death.

Note that the election to use the alternate valuation date generally must be made with the estate tax return. There is, however, a provision that allows for a late-filed election.

The alternate valuation date election can save estate tax, but there’s one potential drawback: The election must be made for the entire estate. In other words, the executor can’t cherry-pick stocks to be valued six months after the date of death and retain the original valuation date for other stocks or assets. It’s all or nothing.

This could be a key consideration if an estate has, for example, sizable real estate holdings in addition to securities. If the real estate has been appreciating in value, making the election may not be the best approach. The executor must conduct a thorough inventory and accounting of the value of all assets.

If your estate includes assets that can fluctuate in value, such as stocks, be sure your executor knows about the option of choosing an alternate valuation date. This option allows flexibility to reduce the chances of estate tax liability. Contact your estate planning advisor for additional information.

© 2022

These days, most businesses buy or lease computer software to use in their operations. Or perhaps your business develops computer software to use in your products or services or sells or leases software to others. In any of these situations, you should be aware of the complex rules that determine the tax treatment of the expenses of buying, leasing or developing computer software.

Some software costs are deemed to be costs of “purchased” software, meaning it’s either:

The entire cost of purchased software can be deducted in the year that it’s placed into service. The cases in which the costs are ineligible for this immediate write-off are the few instances in which 100% bonus depreciation or Section 179 small business expensing isn’t allowed, or when a taxpayer has elected out of 100% bonus depreciation and hasn’t made the election to apply Sec. 179 expensing. In those cases, the costs are amortized over the three-year period beginning with the month in which the software is placed in service. Note that the bonus depreciation rate will begin to be phased down for property placed in service after calendar year 2022.

If you buy the software as part of a hardware purchase in which the price of the software isn’t separately stated, you must treat the software cost as part of the hardware cost. Therefore, you must depreciate the software under the same method and over the same period of years that you depreciate the hardware. Additionally, if you buy the software as part of your purchase of all or a substantial part of a business, the software must generally be amortized over 15 years.

You must deduct amounts you pay to rent leased software in the tax year they’re paid, if you’re a cash-method taxpayer, or the tax year for which the rentals are accrued, if you’re an accrual-method taxpayer. However, deductions aren’t generally permitted before the years to which the rentals are allocable. Also, if a lease involves total rentals of more than $250,000, special rules may apply.

Some software is deemed to be “developed” (designed in-house or by a contractor who isn’t at risk if the software doesn’t perform). For tax years beginning before calendar year 2022, bonus depreciation applies to developed software to the extent described above. If bonus depreciation doesn’t apply, the taxpayer can either deduct the development costs in the year paid or incurred, or choose one of several alternative amortization periods over which to deduct the costs. For tax years beginning after calendar year 2021, generally the only allowable treatment is to amortize the costs over the five-year period beginning with the midpoint of the tax year in which the expenditures are paid or incurred.

If following any of the above rules requires you to change your treatment of software costs, it will usually be necessary for you to obtain IRS consent to the change.

Contact us with questions or for assistance in applying the tax rules for treating computer software costs in the way that is most advantageous for you.

© 2022

How much can you and your employees contribute to your 401(k)s next year — or other retirement plans? In Notice 2022-55, the IRS recently announced cost-of-living adjustments that apply to the dollar limitations for pensions, as well as other qualified retirement plans for 2023. The amounts increased more than they have in recent years due to inflation.

The 2023 contribution limit for employees who participate in 401(k) plans will increase to $22,500 (up from $20,500 in 2022). This contribution amount also applies to 403(b) plans, most 457 plans and the federal government’s Thrift Savings Plan.

The catch-up contribution limit for employees age 50 and over who participate in 401(k) plans and the other plans mentioned above will increase to $7,500 (up from $6,500 in 2022). Therefore, participants in 401(k) plans (and the others listed above) who are 50 and older can contribute up to $30,000 in 2023.

The limitation for defined contribution plans, including a Simplified Employee Pension (SEP) plan, will increase from $61,000 to $66,000. To participate in a SEP, an eligible employee must receive at least a certain amount of compensation for the year. That amount will increase in 2023 to $750 (from $650 for 2022).

Deferrals to a SIMPLE plan will increase to $15,500 in 2023 (up from $14,000 in 2022). The catch-up contribution limit for employees age 50 and over who participate in SIMPLE plans will increase to $3,500 in 2023, up from $3,000.

The IRS also announced that in 2023:

The 2023 limit on annual contributions to an individual IRA will increase to $6,500 (up from $6,000 for 2022). The IRA catch-up contribution limit for individuals age 50 and older isn’t subject to an annual cost-of-living adjustment and will remain $1,000.

Current high inflation rates will make it easier for you and your employees to save much more in your retirement plans in 2023. The contribution amounts will be a great deal higher next year than they’ve been in recent years. Contact us if you have questions about your tax-advantaged retirement plan or if you want to explore other retirement plan options.

© 2022

Companies that wish to reduce their tax bills or increase their refunds shouldn’t overlook the fuel tax credit. It’s available for federal tax paid on fuel used for nontaxable purposes.

The federal fuel tax, which is used to fund highway and road maintenance programs, is collected from buyers of gasoline, undyed diesel fuel, and undyed kerosene. (Dyed fuels, which are limited to off-road use, are exempt from the tax.)

But purchasers of taxable fuel may use it for nontaxable purposes. For example, construction businesses often use gasoline, undyed diesel fuel or undyed kerosene to run off-road vehicles and construction equipment, such as front loaders, bulldozers, cranes, power saws, air compressors, generators and heaters.

As of this writing, a federal fuel tax holiday has been proposed. But even if it’s signed into law (check with your tax advisor for the latest information), businesses can benefit from the fuel tax credit for months the holiday isn’t in effect.

Currently, the federal tax on gasoline is $0.184 per gallon, and the federal tax on diesel fuel and kerosene is $0.244 per gallon. Calculating the fuel tax credit is simply a matter of multiplying the number of gallons used for nontaxable purposes during the year by the applicable rate.

So, for instance, a company that uses 7,500 gallons of gasoline and 15,000 gallons of undyed diesel fuel to operate off-road vehicles and equipment is entitled to a $5,040 credit (7,500 x $0.184) + (15,000 x $0.244).

This may not seem like a large number, but it can add up over the years. And remember, a tax credit reduces your tax liability dollar for dollar. That’s much more valuable than a deduction, which reduces only your taxable income.

Keep in mind, though, that fuel tax credits are includable in your company’s taxable income. That’s because the full amount of the fuel purchases was previously deducted as business expenses, and you can’t claim a deduction and a credit on the same expense.

You can claim the credit by filing Form 4136, “Credit for Federal Tax Paid on Fuels,” with your tax return. If you don’t want to wait until the end of the year to recoup fuel taxes, you can file Form 8849, “Claim for Refund of Excise Taxes,” to obtain periodic refunds.

Alternatively, if your business files Form 720, “Quarterly Federal Excise Tax Return,” you can claim fuel tax credits against your excise tax liability.

No one likes to pay taxes they don’t owe, but if you forgo fuel tax credits, that’s exactly what you’re doing. Given the minimal burden involved in claiming these credits — it’s just a matter of tracking your nontaxable fuel uses and filing a form — there’s really no reason not to do so.

©2022

What makes Roth IRAs so appealing? Primarily, it’s the ability to withdraw money from them tax-free. But to enjoy this benefit, there are a few rules you must follow, including the widely misunderstood five-year rule.

To understand the five-year rule, you first need to understand the three types of funds that may be withdrawn from a Roth IRA:

Contributed principal. This is your after-tax contributions to the account.

Converted principal. This consists of funds that had been in a traditional IRA but that you converted to a Roth IRA (paying tax on the conversion).

Earnings. This includes the (untaxed) returns generated from the contributed or converted principal.

Generally, you can withdraw contributed principal at any time without taxes or early withdrawal penalties, regardless of your age or how long the funds have been held in the Roth IRA. But to avoid taxes and penalties on withdrawals of earnings, you must meet two requirements:

The withdrawal must not be made before you turn 59½, die, become disabled or qualify for an exception to early withdrawal penalties (such as withdrawals for qualified first-time homebuyer expenses), and

You must satisfy the five-year rule.

Withdrawals of converted principal aren’t taxable because you were taxed at the time of the conversion. But they’re subject to early withdrawal penalties if you fail to satisfy the five-year rule.

As the name suggests, the five-year rule requires you to satisfy a five-year holding period before you can withdraw Roth IRA earnings tax-free or converted principal penalty-free. But the rule works differently depending on the type of funds you’re withdrawing.

If you’re withdrawing earnings, the five-year period begins on January 1 of the tax year for which you made your first contribution to any Roth IRA. For example, if you opened your first Roth IRA on April 1, 2018, and treated your initial contribution as one for the 2017 tax year, then the five-year period started on January 1, 2017. That means you were able to withdraw earnings from any Roth IRA tax- and penalty-free beginning on January 1, 2022 (assuming you were at least 59½ or otherwise exempt from early withdrawal penalties).

Note: If you’re not subject to early withdrawal penalties (because, for example, you’re 59½ or older), failure to satisfy the five-year rule won’t trigger a penalty, but earnings will be taxable.

If you’re withdrawing converted principal, the five-year holding period begins on January 1 of the tax year in which you do the conversion. For instance, if you converted a traditional IRA into a Roth IRA at any time during 2017, the five-year period began January 1, 2017, and ended December 31, 2021.

Unlike earnings, however, each Roth IRA conversion is subject to a separate five-year holding period. If you do several conversions over the years, you’ll need to track each five-year period carefully to avoid triggering unexpected penalties.

Keep in mind that the five-year rule only comes into play if you’re otherwise subject to early withdrawal penalties. If you’ve reached age 59½, or a penalty exception applies, then you can withdraw converted principal penalty-free even if the five-year period hasn’t expired.

You may be wondering why the five-year rule applies to withdrawals of funds that have already been taxed. The reason is that the tax benefits of Roth and traditional IRAs are intended to promote long-term saving for retirement. Without the five-year rule, a traditional IRA owner could circumvent the penalty for early withdrawals simply by converting it to a Roth IRA, paying the tax, and immediately withdrawing it penalty-free.

Note, however, that while the five-year rule prevents this, it’s still possible to use a conversion to withdraw funds penalty-free before age 59½. For example, you could convert a traditional IRA to a Roth IRA at age 45, pay the tax, wait five years and then withdraw the converted principal penalty-free.

Generally, one who inherits a Roth IRA may withdraw the funds immediately without fear of taxes or penalties, with one exception: The five-year rule may still apply to withdrawals of earnings if the original owner of the Roth IRA hadn’t satisfied the five-year rule at the time of his or her death.

For instance, suppose you inherited a Roth IRA from your grandfather on July 1, 2021. If he made his first Roth IRA contribution on December 1, 2018, you’ll have to wait until January 1, 2023, before you can withdraw earnings tax-free.

Many people are accustomed to withdrawing retirement savings freely once they reach age 59½. But care must be taken when withdrawing funds from a Roth IRA to avoid running afoul of the five-year rule and inadvertently triggering unexpected taxes or penalties. The rule is complex — so when in doubt, consult a tax professional before making a withdrawal.

The consequences of violating the five-year rule can be costly, but fortunately, there are ordering rules that help you avoid inadvertent mistakes. Under these rules, withdrawals from a Roth IRA are presumed to come from after-tax contributions first, converted principal second, and earnings third.

So, if contributions are large enough to cover the amount you wish to withdraw, you will avoid taxes and penalties even if the five-year rule hasn’t been satisfied for converted principal or earnings. Of course, if you withdraw the entire account balance, the ordering rules won’t help you.

© 2022

A significantly modified update to the Electric Drive Motor Vehicle Credit (IRC Section 30D), went into effect August 17, 2022, and changed this popular tax credit. As of January 1, 2023, the new Clean Vehicle Credit will go into effect. In this article we outline what you need to know about the updated credit.

While the previous credit also allowed up to a $7,500 credit for purchasers of eligible vehicles, it included a maximum manufacturing limit for each car manufacturer. That means General Motors and Tesla brand cars were no longer eligible for the credit. The new version of this tax credit is going to remove this cap but adds several new stipulations that will go into effect over time. In addition, the credit has been expanded to include all clean vehicle types, including plug-in hybrids and hydrogen fuel cell vehicles.

The Department of Entergy (DOE) has given a list of electric vehicles that may meet the updated Electric Drive Motor Vehicle Credit and new Clean Vehicle Credit at https://afdc.energy.gov/laws/inflation-reduction-act. They recommend that taxpayers still confirm that their vehicle meets the new North America assembly requirement.

Suppose you are one of the taxpayers that signed a purchase contract before August 16, 2022 but did not take possession until after August 16, 2022. In that case, you may have the opportunity to choose to use the updated Electric Drive Motor Vehicle Credit rules or be grandfathered into the old tax credit qualifications. This could benefit vehicles by manufacturers that have previously reached their manufacturing cap or for vehicles that do not meet the final assembly requirement. The National Highway Traffic Safety Administration (NHTSA) has a VIN decoder to see if the vehicle qualifies for tax credits.

The State of California does not have a comparable tax credit but offers rebates for purchases of qualified ‘clean vehicles.’ The rebate amounts range from $750 to $7,000 depending on the vehicle and the Manufacturer Suggested Retail Price (MRSP). In addition, low-income families can add up to $2,500 to the rebate for purchasing an eligible vehicle. View the list of vehicles eligible for the California rebate here.

To review your tax planning and whether a clean vehicle purchase would be advantageous, reach out to our team of knowledgeable tax professionals to schedule an appointment.

Many companies are eligible for tax write-offs for certain equipment purchases and building improvements. These write-offs can do wonders for a business’s cash flow, but whether to claim them isn’t always an easy decision. In some cases, there are advantages to following the regular depreciation rules. So it’s critical to look at the big picture and develop a strategy that aligns with your company’s overall tax-planning objectives.

Taxpayers can elect to claim 100% bonus depreciation or Section 179 expensing to deduct the full cost of eligible property up front in the year it’s placed in service. Alternatively, they may spread depreciation deductions over several years or decades, depending on how the tax code classifies the property.

Under the Tax Cuts and Jobs Act (TCJA), 100% bonus depreciation is available for property placed in service through 2022. Without further legislation, bonus depreciation will be phased down to 80% for property placed in service in 2023, 60% in 2024, 40% in 2025, and 20% in 2026; then, after 2026, bonus depreciation will no longer be available. (For certain property with longer production periods, these reductions are delayed by one year. For example, 80% bonus depreciation will apply to long-production-period property placed in service in 2024.)

In March 2020, a technical correction made by the CARES Act expanded the availability of bonus depreciation. Under the correction, qualified improvement property (QIP), which includes many interior improvements to commercial buildings, is eligible for 100% bonus depreciation not only following the phaseout schedule through 2026 but also retroactively to 2018. So, taxpayers that placed QIP in service in 2018 and 2019 may have an opportunity to claim bonus depreciation by amending their returns for those years. If bonus depreciation isn’t claimed, QIP is generally depreciable on a straight-line basis over 15 years.

Sec. 179 also allows taxpayers to fully deduct the cost of eligible property, but the maximum deduction in a given year is $1 million (adjusted for inflation to $1.08 million for 2022), and the deduction is gradually phased out once a taxpayer’s qualifying expenditures exceed $2.5 million (adjusted for inflation to $2.7 million for 2022).

While 100% first-year bonus depreciation or Sec. 179 expensing can significantly lower your company’s taxable income, it’s not always a smart move. Here are three examples of situations where it may be preferable to forgo bonus depreciation or Sec. 179 expensing:

You’re planning to sell QIP. If you’ve invested heavily in building improvements that are eligible for bonus depreciation as QIP and you plan to sell the building in the near future, you may be stepping into a tax trap by claiming the QIP write-off. That’s because your gain on the sale — up to the amount of bonus depreciation or Sec. 179 deductions you’ve claimed — will be treated as “recaptured” depreciation that’s taxable at ordinary-income tax rates as high as 37%. On the other hand, if you deduct the cost of QIP under regular depreciation rules (generally, over 15 years), any long-term gain attributable to those deductions will be taxable at a top rate of 25% upon the building’s sale.

You’re eligible for the Sec. 199A “pass-through” deduction. This deduction allows eligible business owners to deduct up to 20% of their qualified business income (QBI) from certain pass-through entities, such as partnerships, limited liability companies and S corporations, as well as sole proprietorships. The deduction, which is available through 2025 under the TCJA, can’t exceed 20% of an owner’s taxable income, excluding net capital gains. (Several other restrictions apply.)

Claiming bonus depreciation or Sec. 179 deductions reduces your QBI, which may deprive you of an opportunity to maximize the 199A deduction. And since the 199A deduction is scheduled to expire in 2025, it makes sense to take advantage of it while you can.

Your depreciation deductions may be more valuable in the future. The value of a deduction is based on its ability to reduce your tax bill. If you think your tax rate will go up in the coming years, either because you believe Congress will increase rates or you expect to be in a higher bracket, depreciation write-offs may be worth more in future years than they are now.

Keep in mind that forgoing bonus depreciation or Sec. 179 deductions only affects the timing of those deductions. You’ll still have an opportunity to write off the full cost of eligible assets; it will just be over a longer time period. Your tax advisor can analyze how these write-offs interact with other tax benefits and help you determine the optimal strategy for your situation.

©2022

No one needs to remind business owners that the cost of employee health care benefits keeps going up. One way to provide some of these benefits is through an employer-sponsored Health Savings Account (HSA). For eligible individuals, an HSA offers a tax-advantaged way to set aside funds (or have their employers do so) to meet future medical needs. Here are the key tax benefits:

To be eligible for an HSA, an individual must be covered by a “high deductible health plan.” For 2023, a “high deductible health plan” will be one with an annual deductible of at least $1,500 for self-only coverage or at least $3,000 for family coverage. (These amounts in 2022 were $1,400 and $2,800, respectively.) For self-only coverage, the 2023 limit on deductible contributions will be $3,850 (up from $3,650 in 2022). For family coverage, the 2023 limit on deductible contributions will be $7,750 (up from $7,300 in 2022). Additionally, annual out-of-pocket expenses required to be paid (other than for premiums) for covered benefits for 2023 will not be able to exceed $7,500 for self-only coverage or $15,000 for family coverage (up from $7,050 and $14,100, respectively, in 2022).

An individual (and the individual’s covered spouse, as well) who has reached age 55 before the close of the tax year (and is an eligible HSA contributor) may make additional “catch-up” contributions for 2023 of up to $1,000 (unchanged from the 2022 amount).

If an employer contributes to the HSA of an eligible individual, the employer’s contribution is treated as employer-provided coverage for medical expenses under an accident or health plan. It’s also excludable from an employee’s gross income up to the deduction limitation. Funds can be built up for years because there’s no “use-it-or-lose-it” provision. An employer that decides to make contributions on its employees’ behalf must generally make comparable contributions to the HSAs of all comparable participating employees for that calendar year. If the employer doesn’t make comparable contributions, the employer is subject to a 35% tax on the aggregate amount contributed by the employer to HSAs for that period.

HSA withdrawals (or distributions) can be made to pay for qualified medical expenses, which generally means expenses that would qualify for the medical expense itemized deduction. Among these expenses are doctors’ visits, prescriptions, chiropractic care, and premiums for long-term care insurance.

If funds are withdrawn from the HSA for other reasons, the withdrawal is taxable. Additionally, an extra 20% tax will apply to the withdrawal unless it’s made after reaching age 65 or in the event of death or disability.

HSAs offer a flexible option for providing health care coverage, and they may be an attractive benefit for your business. But the rules are somewhat complex. Contact us if you have questions or would like to discuss offering HSAs to your employees.

© 2022

If you need to hire, be aware of a valuable tax credit for employers hiring individuals from one or more targeted groups. The Work Opportunity Tax Credit (WOTC) is generally worth $2,400 for each eligible employee but can be worth more — in some cases, much more.

Generally, an employer is eligible for the credit only for qualified wages paid to members of a targeted group. These groups are:

Employers of all sizes are eligible to claim the WOTC. This includes both taxable and certain tax-exempt employers located in the United States and in some U.S. territories. Taxable employers can claim the WOTC against income taxes. However, eligible tax-exempt employers can claim the WOTC only against payroll taxes and only for wages paid to members of the qualified veteran targeted group.

Many additional conditions must be fulfilled before employers can qualify for the credit. Each employee must have completed a minimum of 120 hours of service for the employer. Also, the credit isn’t available for employees who are related to the employer or who previously worked for the employer.

WOTC amounts differ for specific employees. The maximum credit available for the first year’s wages generally is $2,400 for each employee, or $4,000 for a recipient of long-term family assistance. In addition, for those receiving long-term family assistance, there’s a 50% credit for up to $10,000 of second-year wages. The maximum credit available over two years for these employees is $9,000 ($4,000 for Year 1 and $5,000 for Year 2).

For some veterans, the maximum WOTC is higher: $4,800 for certain disabled veterans, $5,600 for certain unemployed veterans, and $9,600 for certain veterans who are both disabled and unemployed.

For summer youth employees, the wages must be paid for services performed during any 90-day period between May 1 and September 15. The maximum WOTC credit available for summer youth is $1,200 per employee.

Additional rules and requirements apply. For example, you must obtain certification that an employee is a target group member from the appropriate State Workforce Agency before you can claim the credit. The certification generally must be requested within 28 days after the employee begins work. And in limited circumstances, the rules may prohibit the credit or require an allocation of it.

Nevertheless, for most employers that hire from targeted groups, the credit can be valuable. Contact your tax advisor with questions or for more information about your situation.

© 2022

On October 21, 2022, the Internal Revenue Service (IRS) announced the updated contribution limits to retirement plans in Notice 2022-55. The new limits are valid beginning in tax year 2023. These limits are important, as they cap the tax benefits that can be realized from retirement plan savings contributions each year and are adjusted to account for annual inflation.

There are several options available under the ‘Employer Contribution Plans’ category. These plans are typically funded through an employer and may or may not have contributions paid for by the employer. For 401(k), 403(b), the federal government’s Thrift Savings Plan, and most 457 plans, the contribution limit will increase from $20,500 in 2022 to $22,500 in 2023.

Individuals aged 50 years and above can contribute additional funds, called ‘Catch Up Contributions.’ The catch-up contribution limit or the employer-sponsored plans mentioned above will increase from $6,500 in 2022 to $7,500 in 2023. This means those with a qualifying employer-sponsored plan who are 50 or older can contribute up to $30,000 to tax-beneficial retirement plans.

Depending on income, the IRS provides tax benefits to non-employer-sponsored retirement accounts called Individual Retirement Arrangements (IRAs). The traditional IRA offers a deduction for the income in the tax year the contribution is made, while a Roth IRA offers tax benefits when the funds are withdrawn after the qualifying retirement age.

The IRS has increased the contribution limit to these types of accounts to $6,500 in 2023 from $6,000 in 2022. For individuals eligible for a catch-up contribution, the additional contribution amount remains at $1,000.

Keep in mind that there is an income limit on both Traditional IRA and Roth IRA accounts before the tax benefits start to phase out. These limits are:

Traditional IRA |

|

| Single Filers/Heads of Household | $73,000 to $83,000* |

| Married Filing Jointly (spouse contributing covered by employer plan) | $116,000 to $136,000* |

| Married Filing Jointly (contributor not covered by employer plan, but spouse is) | $218,000 to $228,000* |

| Married Filing Separate (contributor covered by an employer plan) | $0 to $10,000* |

Roth IRA |

|

| Single Filers/Heads of Household | $138,000 to $153,000* |

| Married Filing Jointly | $218,000 to $228,000* |

| Married Filing Separate | $0 to $10,000* |

Retirement Savings Contributions Credit |

|

| Single Filers/Married Filing Separate | $36,500 |

| Married Filing Jointly | $73,000 |

| Heads of Household | $54,750 |

*Note: Contribution limits to Traditional IRA and Roth IRA accounts phase out over the noted income range.

Need assistance understanding the tax benefits and contribution limits attached to the different tax-beneficial retirement accounts? Our team of knowledgeable professionals is here to help. Give us a call to discuss your tax strategy for retirement savings today.

The Social Security Administration recently announced that the wage base for computing Social Security tax will increase to $160,200 for 2023 (up from $147,000 for 2022). Wages and self-employment income above this threshold aren’t subject to Social Security tax.

The Federal Insurance Contributions Act (FICA) imposes two taxes on employers, employees, and self-employed workers. One is for the Old Age, Survivors, and Disability Insurance program, which is commonly known as Social Security. The other is for the Hospital Insurance program, which is commonly known as Medicare.

There’s a maximum amount of compensation subject to the Social Security tax, but no maximum for Medicare tax. For 2023, the FICA tax rate for employers is 7.65% — 6.2% for Social Security and 1.45% for Medicare (the same as in 2022).

For 2023, an employee will pay:

For 2023, the self-employment tax imposed on self-employed people is:

What happens if one of your employees works for your business and has a second job? That employee would have taxes withheld from two different employers. Can the employee ask you to stop withholding Social Security tax once he or she reaches the wage base threshold? Unfortunately, no. Each employer must withhold Social Security taxes from the individual’s wages, even if the combined withholding exceeds the maximum amount that can be imposed for the year. Fortunately, the employee will get a credit on his or her tax return for any excess withheld.

Contact us if you have questions about 2023 payroll tax filing or payments. We can help ensure you stay in compliance.

© 2022

Throughout the year, the Federal Emergency Management Agency (FEMA) will designate incidents that adversely affect residents in the affected areas as disasters. This FEMA designation puts relief efforts in motion, both short and long-term.

While immediate needs like food, water, and shelter are at the top of the list, long-term efforts, like relief options through the IRS, aim to help those affected get back on their feet.

In the past, the Senate was required to vote every time the IRS wanted to grant disaster relief provisions to FEMA-designated disaster areas. Now, the IRS can give disaster relief by extending deadlines for “certain time-sensitive acts.” This includes filing returns and paying taxes during the disaster period. For example, affected taxpayers usually receive a tax refund more quickly by “claiming losses related to the disaster on the tax return for the previous year.”

While in some areas of the country, disaster preparedness feels more like a what-if scenario, other parts of the country are all-too-familiar with preparing for floods, wildfires, and tornados. The IRS recommends:

Suppose you or your business have gone through a natural disaster, and you cannot access your original tax documents. In that case, the IRS recommends the following resources for obtaining important financial information when you are ready:

The IRS keeps a list of current and past disaster relief offered on its website. Some of the more recent disaster-related tax relief programs include:

We recommend talking with your tax advisor and visiting the IRS Disaster Relief Website for a comprehensive list.

Even though the overall IRS audit rate is currently low historically, it’s expected to increase as a result of provisions in the Inflation Reduction Act signed into law in August. So it’s more important than ever for taxpayers to follow the rules to minimize their chances of being subject to an audit. How can you reduce your audit chances? Watch for these 10 red flags that can trigger IRS scrutiny:

Of course, this isn’t the end of the list. There are many other potential audit triggers, depending on a taxpayer’s particular situation. Also, keep in mind that some audits are done on a random basis. So even if you have no common triggers on your return, you still could be subject to an audit (though the chances are lower).

With proper tax reporting and professional help, you can reduce the likelihood of triggering an audit. And if you still end up being subject to one, proper documentation can help you withstand it with little or no negative consequences.

©2022

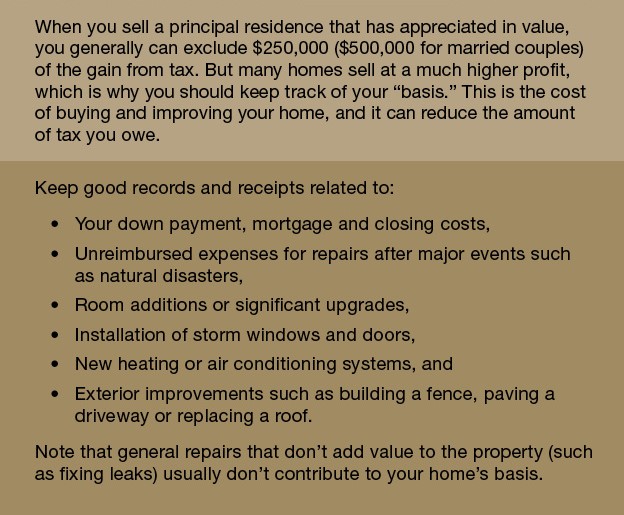

If you’re thinking about selling your home, it’s important to determine whether you qualify for the home sale gain exclusion. The exclusion is one of the most generous tax breaks in the tax code, so be sure to review its requirements before you sell.

Ordinarily, when you sell real estate or other capital assets that you’ve owned for more than one year, your profit is taxable at long-term capital gains rates of 15% or 20%, depending on your tax bracket. High-income taxpayers may also be subject to an additional 3.8% net investment income (NII) tax. If you’re selling your principal residence, however, the home sale gain exclusion may allow you to avoid tax on up to $250,000 in profit for single filers and up to $500,000 for married couples filing jointly.

Don’t assume that you’re eligible for this tax break just because you’re selling your principal residence. If you’re a single filer, to qualify for the exclusion, you must have owned and used the home as your principal residence for at least 24 months of the five-year period ending on the sale date.

If you’re married filing jointly, then both you and your spouse must have lived in the home as your principal residence for 24 months of the preceding five years and at least one of you must have owned it for 24 months of the preceding five years. Special eligibility rules apply to people who become unable to care for themselves, couples who divorce or separate, military personnel, and widowed taxpayers.

You can’t use the exclusion more than once in a two-year period, even if you otherwise meet the requirements. Also, if you convert an ineligible residence into a principal residence and live in it for 24 months or more, only a portion of your gain will qualify for the exclusion.

For example, John is single and has owned a home for five years, using it as a vacation home for the first three years and as his principal residence for the last two. If he sells the home for a $300,000 gain, only 40% of his gain ($120,000) qualifies for the exclusion, and the remaining $180,000 is taxable. (Note: Nonqualified use prior to 2009 doesn’t reduce the exclusion).

What if you sell your home before you meet the 24-month threshold due to a work- or health-related move, or certain other unforeseen circumstances? You may qualify for a partial exclusion.

For example, Paul and Linda bought a home in California for $1 million. One year later, Paul’s employer transferred him to its New York office, so the couple sold the home for $1.2 million. Paul and Linda didn’t meet the 24-month threshold but, because they sold the home due to a work-related move, they qualified for a partial exclusion of 12 months/24 months, or 50%.

Note that the 50% reduction applied to the exclusion, not to the couple’s gain. Thus, their exclusion was reduced to 50% of $500,000, or $250,000, which shielded their entire $200,000 gain from tax.

Before you sell your principal residence, determine the amount of your home sale gain exclusion and your expected gain (selling price less adjusted cost basis). Keep in mind that your cost basis is increased by the cost of certain improvements and other expenses, which in turn reduces your gain. Also, be aware that capital gains attributable to depreciation deductions (for a home office, for example) will be taxable regardless of the home sale gain exclusion.

© 2022

Do you own commercial or investment real estate that has substantially increased in value? If you sell the property, you may be hit with a huge capital gain tax liability. Possible solution: Consider a Section 1031 exchange (also known as a like-kind exchange) in which you swap qualifying properties while paying zero or little current tax.

Recent legislation has narrowed the availability of Sec. 1031 exchanges, but you can still use this technique for qualified real estate transactions. However, keep in mind that a repeal or modification of the rules has been discussed. So, if you’re interested in an exchange, you may want to act soon.

Under Sec. 1031 of the Internal Revenue Code, you can defer tax on the exchange of like-kind real estate properties if specific requirements are met. Previously, this tax break was available for various types of property, such as trade-ins of business vehicles. But as of 2018, the Tax Cuts and Jobs Act strictly limits the Sec. 1031 rules to real estate transactions.

Note that the properties — both the one you relinquish and the one you receive — must be business or investment properties. You can’t avoid current tax if you swap personal residences, but you may be able to exchange a vacation home that is treated as a rental property. (There may be other complications, so consult with your tax advisor.)

Normally, a sale of appreciated real estate would result in capital gains tax. For individual property owners, the maximum tax rate is 20% if the property has been owned for longer than one year. Otherwise, the gain for individuals is taxed at ordinary income tax rates currently topping out at 37%.

If you meet the requirements under Sec. 1031, there’s no current tax due on the exchange — except to the extent that you receive “boot” as part of the deal. Boot includes cash needed to “even things out” or other concessions of value (such as a reduction of mortgage debt). In some cases, cash may be combined with a valued benefit.

If you receive boot, you owe current tax on the amount equal to the lesser of:

On the other hand, if you’re the one paying boot, you won’t realize any taxable gain.

For these purposes, “like-kind” refers to the property’s nature or character. The prevailing tax regulations provide a liberal interpretation of what constitutes like-kind properties. For instance, you can exchange improved real estate for raw land, a strip mall for an apartment building or a marina for a golf course. It doesn’t have to be the exact same type of property (for example, a warehouse for a warehouse).

Timing is everything. The following two deadlines must be met for a like-kind exchange to qualify for tax-free treatment:

The 180-day period begins to run on the date of the transfer of legal ownership of the relinquished property. If that period straddles two tax years, it might be shortened by the tax return due date. So, if you give up title to the property in November or December this year, the due date for 2022 returns (April 18, 2023) would arrive before 180 days are up. Keep this in mind as the end of the year approaches.

Also, in the real world, it’s unlikely that you’ll own property that another person wants to acquire while he or she also owns property that you desire. These one-for-one exchanges are rare. The vast majority of Sec. 1031 real estate exchanges involve multiple parties. (See the sidebar, “Multiple-party exchanges.”)

Unless you’re an expert in the field, a Sec. 1031 exchange is not a do-it-yourself proposition. Enlist the services of professionals, including your CPA, who can provide the assistance you need.

Depending on your situation, you might use a “qualified intermediary” to cement a Section 1031 exchange. Essentially, the qualified intermediary is a third party that helps facilitate the deal. The parties create an agreement whereby the qualified intermediary:

Note that the agreement must limit the taxpayer’s rights to receive, pledge, borrow or otherwise obtain benefits of cash or other property held by the intermediary. In addition, specific IRS reporting requirements must be met. Typically, the intermediary charges a fee based on the value of the properties.

©2022

Businesses can provide benefits to employees that don’t cost them much or anything at all. However, in some cases, employees may have to pay tax on the value of these benefits.

Here are examples of two types of benefits which employees generally can exclude from income:

However, many fringe benefits are taxable, meaning they’re included in the employees’ wages and reported on Form W-2. Unless an exception applies, these benefits are subject to federal income tax withholding, Social Security (unless the employee has already reached the year’s wage base limit) and Medicare.

The line between taxable and nontaxable fringe benefits may not be clear. As illustrated in one recent case, some taxpayers get into trouble if they cross too far over the line.

A retired airline pilot received free stand-by airline tickets from his former employer for himself, his spouse, his daughter, and two other adult relatives. The value of the tickets provided to the adult relatives was valued $5,478. The airline reported this amount as income paid to the retired pilot on Form 1099-MISC, which it filed with the IRS. The taxpayer and his spouse filed a joint tax return for the year in question but didn’t include the value of the free tickets in gross income.

The IRS determined that the couple was required to include the value of the airline tickets provided to their adult relatives in their gross income. The retired pilot argued the value of the tickets should be excluded as a de minimis fringe.

The U.S. Tax Court agreed with the IRS that the taxpayers were required to include in gross income the value of airline tickets provided to their adult relatives. The value, the court stated, didn’t qualify for exclusion as a no-additional-cost service because the adult relatives weren’t the taxpayers’ dependent children. In addition, the value wasn’t excludable under the tax code as a de minimis fringe benefit “because the tickets had a value high enough that accounting for their provision was not unreasonable or administratively impracticable.” (TC Memo 2022-36)

You may be able to exclude from wages the value of certain fringe benefits that your business provides to employees. But the requirements are strict. If you have questions about the tax implications of fringe benefits, contact us.

© 2022

You and your small business are likely to incur a variety of local transportation costs each year. There are various tax implications for these expenses.

First, what is “local transportation?” It refers to travel in which you aren’t away from your tax home (the city or general area in which your main place of business is located) long enough to require sleep or rest. Different rules apply if you’re away from your tax home for significantly more than an ordinary workday and you need sleep or rest in order to do your work.

The most important feature of the local transportation rules is that your commuting costs aren’t deductible. In other words, the fare you pay or the miles you drive simply to get to work and home again are personal and not business miles. Therefore, no deduction is available. This is the case even if you work during the commute (for example, via a cell phone, or by performing business-related tasks while on the subway).

An exception applies for commuting to a temporary work location that’s outside of the metropolitan area in which you live and normally work. “Temporary,” for this purpose, means a location where your work is realistically expected to last (and does in fact last) for no more than a year.

On the other hand, once you get to the work location, the cost of any local trips you take for business purposes is a deductible business expense. So, for example, the cost of travel from your office to visit a customer or pick up supplies is deductible. Similarly, if you have two business locations, the costs of traveling between them is deductible.

If your deductible trip is by taxi or public transportation, save a receipt if possible or make a notation of the expense in a logbook. Record the date, amount spent, destination, and business purpose. If you use your own car, note miles driven instead of the amount spent. Note also any tolls paid or parking fees and keep receipts.

You’ll need to allocate your automobile expenses between business and personal use based on miles driven during the year. Proper recordkeeping is crucial in the event the IRS challenges you.

Your deduction can be computed using:

From 2018 – 2025, employees, may not deduct unreimbursed local transportation costs. That’s because “miscellaneous itemized deductions” — a category that includes employee business expenses — are suspended (not allowed) for 2018 through 2025. However, self-employed taxpayers can deduct the expenses discussed in this article. But beginning with 2026, business expenses (including unreimbursed employee auto expenses) of employees are scheduled to be deductible again, as long as the employee’s total miscellaneous itemized deductions exceed 2% of adjusted gross income.

Contact us with any questions or to discuss the matter further.

© 2022

Estate planning usually starts with a Last Will and Testament, a legal document that spells out how you want your assets to be distributed and other affairs handled after you die. A will is a good first step in estate planning, but it’s not necessarily the best option in every situation.

For California residents, trusts can be especially beneficial. In this article, we’ll discuss why you might want to consider setting up a trust or updating your existing trust if you haven’t looked at it in a while.

While there are many different kinds of trusts, a living trust is one of the most popular types for estate planning.

A living trust is a legal entity that distributes your property to people and organizations after you pass away. Once you establish a living trust, you fund it by putting your assets in the trust’s name. You can put all kinds of assets into a living trust, including real estate, investments, stock from closely held corporations, certificates of deposit (CDs), life insurance, personal property, collectibles, and more.

Living trusts may be revocable or irrevocable. Revocable trusts are more popular for estate planning, as they’re flexible and can be changed any time during your lifetime (as long as you are competent). Irrevocable trusts typically can’t be changed without a court order or approval of the trust’s beneficiaries.

Revocable living trusts are particularly beneficial for California residents for two main reasons.

Currently, probate is generally required for all estates in California valued at more than $184,500 unless all the assets are in a trust. (For deaths prior to April 1, 2022, the maximum value of an estate was $166,250.) There are a few exceptions. For example, property owned jointly automatically transfers to the surviving owner, and life insurance policies and retirement accounts go to the beneficiaries, as long as they are correctly designated.

Other assets must go through probate, including real estate, personal property, and bank and investment accounts. In California, anyone can view probate records, so setting up a trust can help you and your loved ones maintain privacy.

Probate attorney fees are set by statute in California, and they’re based on a percentage of the value of assets that go through probate.

Currently, those rates are:

For value above $25 million, the court determines a “reasonable amount.”

California real estate is expensive so going through probate can be costly based on the value of a residence alone.

For example, say you own a home valued at $1,000,000—roughly the median home price in San Diego. Based on the value of your residence alone, your estate’s probate fees would be:

The attorney’s statutory fee would be $23,000, even if they just file paperwork.

This fee applies even if the home is fully mortgaged since it’s based on the gross amount of probate assets.

If you already have a trust but haven’t looked at it in a while, now is a good time to review it with your attorney.

Many life events can impact how you want to distribute your estate, so it’s essential to ensure your trust and other estate planning documents are up to date.

In general, we recommend reviewing your trust every three to five years or after any of the following life events:

We also recommend working with an estate planning attorney to draft or revise a trust. Many clients think they can save money by using a trust form found on the internet, but estate planning is complex, and trusts are governed by state law. The short-term savings from a DIY approach aren’t worth the expensive problems it can create down the road.

If you’d like a referral to an estate planning attorney, would like us to review your trust documents for tax consequences, or need help with a trust tax return, reach out to a Hamilton Tharp advisor.

IRS audit rates are historically low, according to a recent Government Accountability Office (GAO) report, but that’s little consolation if your return is among those selected to be examined. Plus, the IRS recently received additional funding in the Inflation Reduction Act to improve customer service, upgrade technology and increase audits of high-income taxpayers. But with proper preparation and planning, you should fare well.

From tax years 2010 to 2019, audit rates of individual tax returns decreased for all income levels, according to the GAO. On average, the audit rate for all returns decreased from 0.9% to 0.25%. IRS officials attribute this to reduced staffing as a result of decreased funding. Businesses, large corporations, and high-income individuals are more likely to be audited, but overall, all types of audits are being conducted less frequently than they were a decade ago.

There’s no 100% guarantee that you won’t be picked for an audit because some tax returns are chosen randomly. However, the best way to survive an IRS audit is to prepare in advance. On an ongoing basis, you should systematically maintain documentation — invoices, bills, canceled checks, receipts, or other proof — for all items to be reported on your tax returns. Keep all records in one place.

It also helps to know what might catch the attention of the IRS. Certain types of tax-return entries are known to involve inaccuracies, so they may lead to an audit. Here are a few examples:

Certain types of deductions may be questioned by the IRS because there are strict recordkeeping requirements for them — for example, auto and travel expense deductions. In addition, an owner-employee’s salary that’s much higher or lower than those at similar companies in his or her location may catch the IRS’s eye, especially if the business is structured as a corporation.

If you’re selected for an audit, you’ll be notified by letter. Generally, the IRS doesn’t make initial contact by phone. But if there’s no response to the letter, the agency may follow up with a call.

Many audits simply request that you mail in documentation to support certain deductions you’ve claimed. Only the strictest version, the field audit, requires meeting with one or more IRS auditors. (Note: Ignore unsolicited emails or text messages about an audit. The IRS doesn’t contact people in this manner. These are scams.)

The tax agency doesn’t demand an immediate response to a mailed notice. You’ll be informed of the discrepancies in question and given time to prepare. Collect and organize all relevant income and expense records. If anything is missing, you’ll have to reconstruct the information as accurately as possible based on other documentation.

If you’re audited, our firm can help you:

The IRS normally has three years within which to conduct an audit, and an audit probably won’t begin until a year or more after you file a return. Don’t panic if the IRS contacts you. Many audits are routine. By taking a meticulous, proactive approach to tracking, documenting and filing your company’s tax-related information, you’ll make an audit less painful and even decrease the chances you’ll be chosen in the first place.

© 2022

Does your business need real estate to conduct operations? Or does it otherwise hold property and put the title in the name of the business? You may want to rethink this approach. Any short-term benefits may be outweighed by the tax, liability, and estate planning advantages of separating real estate ownership from the business.

Businesses that are formed as C corporations treat real estate assets as they do equipment, inventory and other business assets. Any expenses related to owning the assets appear as ordinary expenses on their income statements and are generally tax deductible in the year they’re incurred.

However, when the business sells the real estate, the profits are taxed twice — at the corporate level and at the owner’s individual level when a distribution is made. Double taxation is avoidable, though. If ownership of the real estate were transferred to a pass-through entity instead, the profit upon sale would be taxed only at the individual level.

Separating your business ownership from its real estate also provides an effective way to protect it from creditors and other claimants. For example, if your business is sued and found liable, a plaintiff may go after all of its assets, including real estate held in its name. But plaintiffs can’t touch property owned by another entity.

The strategy also can pay off if your business is forced to file for bankruptcy. Creditors generally can’t recover real estate owned separately unless it’s been pledged as collateral for credit taken out by the business.

Separating real estate from a business may give you some estate planning options, too. For example, if the company is a family business but some members of the next generation aren’t interested in actively participating, separating property gives you an extra asset to distribute. You could bequest the business to one heir and the real estate to another family member who doesn’t work in the business.

The business simply transfers ownership of the real estate and the transferee leases it back to the company. Who should own the real estate? One option: The business owner could purchase the real estate from the business and hold title in his or her name. One concern is that it’s not only the property that’ll transfer to the owner, but also any liabilities related to it.

Moreover, any liability related to the property itself could inadvertently put the business at risk. If, for example, a client suffers an injury on the property and a lawsuit ensues, the property owner’s other assets (including the interest in the business) could be in jeopardy.

An alternative is to transfer the property to a separate legal entity formed to hold the title, typically a limited liability company (LLC) or limited liability partnership (LLP). With a pass-through structure, any expenses related to the real estate will flow through to your individual tax return and offset the rental income.

An LLC is more commonly used to transfer real estate. It’s simple to set up and requires only one member. LLPs require at least two partners and aren’t permitted in every state. Some states restrict them to certain types of businesses and impose other restrictions.

Separating the ownership of a business’s real estate isn’t always advisable. If it’s worthwhile, the right approach will depend on your individual circumstances. Contact us to help determine the best approach to minimize your transfer costs and capital gains taxes while maximizing other potential benefits.

© 2022

In today’s tough job market and economy, the Work Opportunity Tax Credit (WOTC) may help employers. Many business owners are hiring and should be aware that the WOTC is available to employers that hire workers from targeted groups who face significant barriers to employment. The credit is worth as much as $2,400 for each eligible employee ($4,800, $5,600, and $9,600 for certain veterans and $9,000 for “long-term family assistance recipients”). It’s generally limited to eligible employees who begin work for the employer before January 1, 2026.

The IRS recently issued some updated information on the pre-screening and certification processes. To satisfy a requirement to pre-screen a job applicant, a pre-screening notice must be completed by the job applicant and the employer on or before the day a job offer is made. This is done by filing Form 8850, Pre-Screening Notice, and Certification Request for the Work Opportunity Credit.

An employer is eligible for the credit only for qualified wages paid to members of a targeted group. These groups are:

There are a number of requirements to qualify for the credit. For example, there’s a minimum requirement that each employee must have completed at least 120 hours of service for the employer. Also, the credit isn’t available for certain employees who are related to or who previously worked for the employer.

There are different rules and credit amounts for certain employees. The maximum credit available for the first-year wages is $2,400 for each employee, $4,000 for long-term family assistance recipients, and $4,800, $5,600, or $9,600 for certain veterans. Additionally, for long-term family assistance recipients, there’s a 50% credit for up to $10,000 of second-year wages, resulting in a total maximum credit of $9,000 over two years.

For summer youth employees, the wages must be paid for services performed during any 90-day period between May 1 and September 15. The maximum WOTC credit available for summer youth employees is $1,200 per employee.

In some cases, employers may elect not to claim the WOTC. And in limited circumstances, the rules may prohibit the credit or require an allocation of it. However, for most employers hiring from targeted groups, the credit can be beneficial. Contact us with questions or for more information about your situation.

© 2022

While the new research and development tax credit requirements went into effect on January 10, 2022, which require more detailed proof that claims are valid, many businesses seeking the refund may face extra work when applying for the credit on their next tax return.

Knowing the credit’s specificity requirements will allow businesses to ensure sufficient information is collected and filed with amended tax returns to provide proof for the claim. Putting processes in place to record these requirements throughout the year can help lessen the paperwork burden around tax time.

Any business submitting an R&D tax credit claim must include detailed information about the funds for which they are requesting the credit and the business components related to the claim for the associated tax year.

For each business component, answer the following questions in detail:

The IRS has granted flexibility in how the information is presented, so businesses can use a list, table, or narrative.

In addition to the above questions, the IRS requires a business to provide tax-year totals for:

These expenses are outlined on Form 6765 (Credit for Increasing Research Activities) and must be completed appropriately to qualify for the credit.

The final piece of information the IRS requires is a signed declaration verifying that all facts provided in the report and on the tax forms are accurate.

If the IRS finds information is missing or requires additional clarification, it will request what is needed by letter. Businesses and taxpayers have 45 days from being notified, instead of the traditional 30 days, to remedy the situation.

If the business misses the window or does not provide sufficient information at that point, the IRS can deny the R&D tax credit claim.

After January 9, 2023, the IRS will no longer allow a perfection period. This mean means claims must be complete and accurate when submitted; otherwise, they are considered untimely if corrected after the deadline. The IRS advises that “taxpayers should take extra precaution to substantiate their credit for a refund claim.”

For assistance with the new research and development tax credit requirements as they apply to your business, reach out to our team to set up a time for a consultation.

Here are some of the key tax-related deadlines affecting businesses and other employers during the fourth quarter of 2022. Keep in mind that this list isn’t all-inclusive, so there may be additional deadlines that apply to you. Contact us to ensure you’re meeting all applicable deadlines and to learn more about the filing requirements.

Note: Certain tax-filing and tax-payment deadlines may be postponed for taxpayers who reside in or have businesses in federally declared disaster areas.

The last day you can initially set up a SIMPLE IRA plan, provided you (or any predecessor employer) didn’t previously maintain a SIMPLE IRA plan. If you’re a new employer that comes into existence after October 1 of the year, you can establish a SIMPLE IRA plan as soon as administratively feasible after your business comes into existence.

Contact us if you’d like more information about the filing requirements and to ensure you’re meeting all applicable deadlines.

© 2022

Now that Labor Day has passed, it’s a good time to think about making moves that may help lower your small business taxes for this year and next. The standard year-end approach of deferring income and accelerating deductions to minimize taxes will likely produce the best results for most businesses, as will bunching deductible expenses into this year or next to maximize their tax value.

If you expect to be in a higher tax bracket next year, opposite strategies may produce better results. For example, you could pull income into 2022 to be taxed at lower rates, and defer deductible expenses until 2023, when they can be claimed to offset higher-taxed income.

Here are some other ideas that may help you save tax dollars if you act before year-end.

Taxpayers other than corporations may be entitled to a deduction of up to 20% of their qualified business income (QBI). For 2022, if taxable income exceeds $340,100 for married couples filing jointly (half that amount for others), the deduction may be limited based on: whether the taxpayer is engaged in a service-type business (such as law, health or consulting), the amount of W-2 wages paid by the business, and/or the unadjusted basis of qualified property (such as machinery and equipment) held by the business. The limitations are phased in.

Taxpayers may be able to salvage some or all of the QBI deduction by deferring income or accelerating deductions to keep income under the dollar thresholds (or be subject to a smaller deduction phaseout). You also may be able increase the deduction by increasing W-2 wages before year-end. The rules are complex, so consult us before acting.

More small businesses are able to use the cash (rather than the accrual) method of accounting for federal tax purposes than were allowed to do so in previous years. To qualify as a small business under current law, a taxpayer must (among other requirements) satisfy a gross receipts test. For 2022, it’s satisfied if, during a three-year testing period, average annual gross receipts don’t exceed $27 million. Not that long ago, it was only $5 million. Cash method taxpayers may find it easier to defer income by holding off billings until next year, paying bills early or making certain prepayments.

Consider making expenditures that qualify for the Section 179 expensing option. For 2022, the expensing limit is $1.08 million, and the investment ceiling limit is $2.7 million. Expensing is generally available for most depreciable property (other than buildings) including equipment, off-the-shelf computer software, interior improvements to a building, HVAC and security systems.

The high dollar ceilings mean that many small- and medium-sized businesses will be able to currently deduct most or all of their outlays for machinery and equipment. What’s more, the deduction isn’t prorated for the time an asset is in service during the year. Just place eligible property in service by the last days of 2022 and you can claim a full deduction for the year.

Businesses also can generally claim a 100% bonus first year depreciation deduction for qualified improvement property and machinery and equipment bought new or used, if purchased and placed in service this year. Again, the full write-off is available even if qualifying assets are in service for only a few days in 2022.

Consult With Us for More Ideas

These are just some year-end strategies that may help you save taxes. Contact us to tailor a plan that works for you.

© 2022

The business entity you choose can affect your taxes, your personal liability, and other issues. A limited liability company (LLC) is somewhat of a hybrid entity in that it can be structured to resemble a corporation for owner liability purposes and a partnership for federal tax purposes. This duality may provide you with the best of both worlds.

Like the shareholders of a corporation, the owners of an LLC (called “members” rather than shareholders or partners) generally aren’t liable for business debts except to the extent of their investment. Thus, they can operate the business with the security of knowing that their personal assets are protected from the entity’s creditors. This protection is far greater than that afforded by partnerships. In a partnership, the general partners are personally liable for the debts of the business. Even limited partners, if they actively participate in managing the business, can have personal liability.