The IRS has released additional guidance in Notice 2021-20 on the Employee Retention Tax Credit (ERC) with clarifications on the retroactive changes for expanded eligibility applicable to 2020. Employers who received a Paycheck Protection Program (PPP) loan have been waiting on guidance on claiming the credit in combination with forgiveness of their loan. The provisions outlined here apply to retroactive claims for 2020 as well as providing a plan for those yet to seek forgiveness.

Summary of ERC

As a reminder, eligibility to claim the 2020 ERC requires a business to have experienced a significant decline in revenues during 2020. Specifically, gross receipts for a calendar quarter during 2020 must have declined by 50% or more when compared to the same calendar quarter in 2019. Additionally, a company is eligible during any period where operations were suspended due to a government order.

Employers with more than 100 FTEs can only claim the ERC on employees that are being paid qualified wages and not providing services.

For 2020, the credit is available on 50% of qualified wages up to $10,000. The maximum credit amount per employee is $5,000.

Health care costs are included when determining qualified wages.

Wages paid as a result of the Families First Coronavirus Response Act (FFCRA) do not qualify.

Clarification on how to apply ERC with a PPP loan

The notice clarifies when and how PPP borrowers can claim the ERC on 2020 wages.

Wages elected to be covered by the PPP forgiveness application but not granted.

Wages in excess of the amount of their PPP loan – Example: An employer receives a $200,000 loan for wages but pays $230,000 in wages. Apply the $30,000 wages to ERC.

The difference in wages and nonpayroll costs that are in excess of their PPP loan – Example: If a PPP loan equals $200,000 and the employer has $200,000 in forgivable wages and $70,000 in forgivable nonpayroll costs, reserve $70,000 in wages for ERC.

Those that have already applied for forgiveness cannot amend their application to claim nonpayroll costs.

For those yet to apply for forgiveness and eligible for the ERC, you will want to accumulate and submit nonpayroll costs to maximize eligible wages for the ERC.

The ERC requires specific documentation and support of facts and circumstances in order to qualify and receive the credit. For assistance with claiming the ERC, contact us.

Merger and acquisition activity in many industries slowed during 2020 due to COVID-19. But analysts expect it to improve in 2021 as the country comes out of the pandemic. If you are considering buying or selling another business, it’s important to understand the tax implications.

Two ways to arrange a deal

Under current tax law, a transaction can basically be structured in two ways:

1. Stock (or ownership interest). A buyer can directly purchase a seller’s ownership interest if the target business is operated as a C or S corporation, a partnership, or a limited liability company (LLC) that’s treated as a partnership for tax purposes.

The current 21% corporate federal income tax rate makes buying the stock of a C corporation somewhat more attractive. Reasons: The corporation will pay less tax and generate more after-tax income. Plus, any built-in gains from appreciated corporate assets will be taxed at a lower rate when they’re eventually sold.

The current law’s reduced individual federal tax rates have also made ownership interests in S corporations, partnerships and LLCs more attractive. Reason: The passed-through income from these entities also is taxed at lower rates on a buyer’s personal tax return. However, current individual rate cuts are scheduled to expire at the end of 2025, and, depending on actions taken in Washington, they could be eliminated earlier.

Keep in mind that President Biden has proposed increasing the tax rate on corporations to 28%. He has also proposed increasing the top individual income tax rate from 37% to 39.6%. With Democrats in control of the White House and Congress, business and individual tax changes are likely in the next year or two.

2. Assets. A buyer can also purchase the assets of a business. This may happen if a buyer only wants specific assets or product lines. And it’s the only option if the target business is a sole proprietorship or a single-member LLC that’s treated as a sole proprietorship for tax purposes.

Preferences of buyers

For several reasons, buyers usually prefer to buy assets rather than ownership interests. In general, a buyer’s primary goal is to generate enough cash flow from an acquired business to pay any acquisition debt and provide an acceptable return on the investment. Therefore, buyers are concerned about limiting exposure to undisclosed and unknown liabilities and minimizing taxes after a transaction closes.

A buyer can step up (increase) the tax basis of purchased assets to reflect the purchase price. Stepped-up basis lowers taxable gains when certain assets, such as receivables and inventory, are sold or converted into cash. It also increases depreciation and amortization deductions for qualifying assets.

Preferences of sellers

In general, sellers prefer stock sales for tax and nontax reasons. One of their objectives is to minimize the tax bill from a sale. That can usually be achieved by selling their ownership interests in a business (corporate stock or partnership or LLC interests) as opposed to selling assets

With a sale of stock or other ownership interest, liabilities generally transfer to the buyer and any gain on sale is generally treated as lower-taxed long-term capital gain (assuming the ownership interest has been held for more than one year).

Obtain professional advice

Be aware that other issues, such as employee benefits, can also cause tax issues in M&A transactions. Buying or selling a business may be the largest transaction you’ll ever make, so it’s important to seek professional assistance. After a transaction is complete, it may be too late to get the best tax results. Contact us about how to proceed.

Last spring, the CARES Act created the ERC for businesses that were affected by the COVID-19 pandemic. However, the CARES Act disallowed the credit for businesses that received a Paycheck Protection Program (PPP) loan. Fast forward to December 2020, when Congress declared that businesses that had obtained PPP loans could also qualify for the ERC. In addition, Congress extended the availability of the ERC into the first two quarters of 2021, with a few new favorable provisions. The credit is refundable, which means that qualified businesses are able to get cash to the extent that the credit exceeds the payroll tax liabilities. The chart below outlines the terms of the ERC for both the original and extended filing periods:

How does PPP loan forgiveness impact the ERC?

In a statement from the Internal Revenue Service (IRS), “[t]he eligible employer can claim the ERC on any qualified wages that are not counted as payroll costs in obtaining PPP loan forgiveness. Any wages that could count toward eligibility for the ERC or PPP loan forgiveness can be applied to either of these two programs, but not both.” The release of the new loan forgiveness applications on January 19, 2021, includes a provision to incorporate this change in guidance on a forward-looking basis. The revised loan forgiveness applications (Form 3508S, Form 3508EZ and Form 3508) note that a borrower should “not include qualified wages taken into account in determining the Employee Retention Credit.”

My PPP loan was already forgiven, what now?

As I previously noted, a business cannot “double dip,” or utilize the same wages to obtain PPP loan forgiveness while still benefiting from the ERC. However, the ERC was not available to PPP recipients prior to December 27, 2020. Accordingly, those businesses that applied for loan forgiveness would have included all eligible payroll costs paid or incurred during the covered period pursuant to the instructions in the loan forgiveness applications. Certainly, those businesses shouldn’t be penalized for already receiving forgiveness prior to this change in the law; however, this wouldn’t be the first time we’ve seen something like that with the evolution of the PPP.

On January 15, the American Institute of Certified Public Accountants (AICPA) sought clarification on this matter. In a letter to the IRS, the AICPA “recommends that the IRS and Treasury provide guidance stating that the filing of a PPP loan forgiveness application does not constitute an election to forgo the ERC with respect to the amount of wages reported on the application exceeding the amount of wages necessary for loan forgiveness.” It is clear — additional guidance is imminent.

What’s next?

As we await clarification from the IRS, businesses who have already received forgiveness on their PPP loans should first evaluate their eligibility for the ERC. After concluding their eligibility, businesses should begin gathering payroll reports, government shutdown orders and financial statements to calculate and claim their credits.

Borrowers of PPP loans who have yet to apply for loan forgiveness have an alternative path; those businesses looking to leverage the ERC now have an additional element to consider in their evolving journey to loan forgiveness. This change in guidance further emphasizes the importance of an intentional strategy to maximize the benefits of both programs, but also leaves questions unanswered for borrowers who have already received forgiveness on their PPP loans.

The Internal Revenue Service recently issued the 2021 optional standard mileage rates. These rates, which adjust every year to account for inflation of fuel costs, vehicle cost and maintenance, and insurance rate increases, will once again affect the way a company reimburses their mobile workers. Specifically, the IRS mileage rate is a guideline that businesses use to calculate the deductible costs of operating an automobile for business, charitable, medical, or moving purposes. Beyond announcing the rate change, we have a few reminders and tips surrounding this reimbursement allowance.

As of January 1, 2021, the standard mileage rates for the use of a car (also vans, pickups or panel trucks) are:

56 cents per mile for business miles driven, down1.5 cents from 2020

16 cents per mile driven for medical or moving purposes, down1cent from 2020

14 cents per mile driven in service of charitable organizations; the mileage rate for service to a charitable organization is not alterable by the IRS. Instead, it must be changed by a Congress -passed statute.

Have you considered…

Under the Tax Cuts and Jobs Act, employees are not permitted to write off unreimbursed business mileage. If your company does not make up for this reimbursement, it could face legal consequences.

A taxpayer may not use the business standard mileage rate for a vehicle after using any depreciation method under the Modified Accelerated Cost Recovery System (MACRS) or after claiming a Section 179 deduction for that vehicle.

Taxpayers alsohave the option of calculating the actual costs of using their vehicle rather than using the standard mileage rates. The actual expense method often produces a significantly different result. You will want to talk with your CPA to determine which method yields the larger deduction.

Remember,

The IRS rate was intended to function as a reimbursement cap. Today, the rate holds businesses accountable, but it doesn’t account for fluctuations in vehicle prices across city, county, and state lines. For companies whoseemployees use their vehicles for work, there is an alternative to the standard mileage rate. The Fixed and Variable Rate (FAVR) allowance preserves reimbursement equity and helps businesses avoid over- or underpayment to employees. To find out more about this IRS recommended reimbursement methodology or if you have any questions about the IRS Standard Mileage Rate, please contact one of our professionals today.

The employee retention tax credit (ERTC) is intended to provide liquidity to employers during the pandemic and was greatly expanded in the Consolidated Appropriations Act of 2021 thanks to Sections 206 and 207 of the Taxpayer Certainty and Disaster Relief Act portion, opening the doors to more businesses to be able to qualify for and receive this credit who are facing significant hardship as a result of the coronavirus pandemic. Many changes from the original credit were enacted including an expansion in the amount of credit and business eligibility, and how it plays with the Paycheck Protection Program (PPP).

Here’s what you need to know about this credit, how it works, and how to apply. Note that when a provision is designated as effective Jan. 1, 2021, it does not apply to any retroactive credit claims.

Who is eligible for the ERTC?

The following businesses and organizations engaged in a trade or business are eligible to qualify for the ERTC:

For-profit businesses

Tax-exempt organizations

Certain government entities that are state or local-run (Effective Jan. 1, 2021, previously no government entity at any level was eligible):

Colleges or universities

Organizations providing medical or hospital care

Certain organizations charted by Congress (such as Fannie Mae, FDIC, Federal Home Loan Banks and Federal Credit Unions)

How does my business qualify for the ERTC?

An eligible organization can qualify for the ERTC if:

Their operations are fully or partially suspended due to a lockdown order, OR

Their gross receipts are less than 80% for a quarter in 2021 or the immediately compared to the same quarter in 2019 (or 2020 if the business was not open in 2019) or, there is a 20% drop quarter-over-quarter when comparing Q1 of 2021 to Q4 of 2020 compared to Q4 of 2019.

The gross receipts test is Effective Jan. 1, 2021, this is an increase from the previous law and expands the threshold for eligible businesses.

Effective Jan. 1, 2021, businesses with 500 employees or less are eligible to claim the credit even if an employee is working during the first two quarters of 2021 (an increase in the threshold from 100 employees in the original law). For affiliated companies sharing more than 50% common ownership, the 500 count is aggregated.

What is the time period for the credit, and when can I start collecting?

The passage of the bill at the end of December extended the availability of the ERTC through the first two quarters of 2021, allowing for more relief as the pandemic continues on. Qualified wages paid after March 12, 2020, and before July 1, 2021, are eligible for the credit.

Additionally, the new law will allow for an advanced credit for companies with 500 or fewer employees, allowing these companies to monetize the credit before wages are paid. The amount is based on 70% of the average quarterly payroll for the same quarter in 2019, and if there is excess advance payment, companies will need to repay the credit to the government.

How much credit can I receive?

Effective Jan. 2021, 70% of qualified wages are eligible for the ERTC including the cost to continue providing health benefits (such as if an employee is on furlough). This is an increase from the 50% provided in the previous stimulus bill. The qualified wage limit was increased to $10,000 per quarter per employee for the first 2 quarters of 2020. Previously was $10,000 per employee for the entirety of 2020.

Also, effective Jan. 1, 2021, the credit maxes out at an aggregate $14,000 per employee, or $7,000 for the first two quarters of 2021, and is available even if the employer received the maximum credit for wages paid to the same employee in 2020. This is an increase from the $5,000 max in the previous bill.

Additionally, the credit is now available for certain pay raises including hazardous duty pay increases (previously not allowed and is retroactive).

How does my PPP loan factor in?

First and foremost, companies with PPP loans can now also claim the ERTC, and the change is retroactive to the effective date of the original law (March 12, 2020). Key to note is that the ERTC cannot be applied toward wages covered by the PPP.

If, for example, your business received a PPP loan in 2020 and paid qualified wages in excess of the PPP loan amount, you could qualify and apply for the ERTC through an amended employment tax return (Forms 941X). This also applies to affiliate companies related to a PPP borrower. Furthermore, if your PPP payroll costs are not forgiven, those same payroll costs can be applied toward ERTC qualified wages. Your accountant can help you calculate and designate these costs.

Claiming the ERTC, with or without a PPP loan, requires careful calculation and documentation. Contact us for assistance with this credit.

The U.S. House of Representatives and U.S. Senate have passed the Coronavirus Response & Relief Supplemental Appropriations Act, and President Trump is expected to sign the bill immediately. The agreement comes after weeks of negotiations and two funding extensions to keep Congress open until a bill was passed with a $1.4 trillion government-wide funding plan. The $900 billion coronavirus relief portion includes another round of Paycheck Protection Program (PPP) funding, extended unemployment benefits, and direct payments to taxpayers. Here’san overview of the key provisions in the bill.

Updates to the PPP and changes for second round

The Act designates $267.5 billion for this round of PPP funding, and the program specifically sets aside $25 billion for businesses with 10 employees or less as of Feb. 15, 2020. Regulations for this round of PPP funding are required to be released within 10 days of enactment.

Borrowers who received PPP funding in the first round following the CARES Act will receive some additional updates to their existing PPP loans. Borrowers who would like to adjust their requested loan amount based on these updated regulations may do so, provided they have not yet received forgiveness. Here are the key updates:

More expenses are eligible – Covered operations expenditures (including business software and cloud computing services), property damage costs (costs incurred during public disturbances in 2020 not covered by insurance), supplier costs (that are essential to operations), and worker protection expenditures (to comply with HHS, CDC, or OSHA requirements) would be eligible for forgiveness. These amendments would not apply to loans that have already been forgiven.

Tax deductions on related expenses are allowed – The bill reverses an earlier ruling and makes expenses deductible. It also confirms forgiveness is non-taxable.

Loans up to $150,000 get a simplified forgiveness application process –Borrowers with loans up to $150,000 will get one-page online or paper form with borrower certifications of the number employees covered by the loan, the estimated amount spent on payroll, and the total amount of the loan. Borrowers must still maintain appropriate documentation.

Borrowers do not have to deduct EIDL advance – Previously, EIDL advances were to be deducted from the PPP forgiveness amount, but that was repealed.

PPP borrowers can also get an Employee Retention Credit–Wages used for ERC will not be eligible for PPP forgiveness.

The second round of funding provided by this Act has a few key differences from the first round in the CARES Act. Key to note is that borrowers can apply for a second PPP loan through this program if they have fully used their first PPP loan and meet the employer size and gross revenue criteria listed below. PPP loans in this round are capped at $2 million. Here are the key differences:

Changes to employer size and gross revenue qualifications – Only businesses with up to 300 employees (down from 500 employees) and a gross revenue decline by at least 25% for any quarter of 2020 compared to the same quarter in 2019 will qualify for this round.

Changes to loan limits – The loan amount is limited to 2.5 times of the average payroll for the last 12 months through date of application or 2019 and is limited to $2 million. Businesses that are part of the NAICS code beginning with 72 – Accommodation and Food Services – are limited to 3.5 times payroll for the 1-year period or 2019 and limited to $2 million.

Changes to eligible nonprofits – 501(c)(6)s now qualify – These organizations must have 150 employees or fewer, gross receipts from lobbying activities must total less than 15% or $1 million, and lobbying activities cannot comprise more than 15% of total activities.

More groups can apply for first-time assistance – Other groups that can apply for first-time assistance through this round of PPP funding include businesses eligible for other SBA 7(a) loans with fewer than 500 employees, sole proprietors, independent contractors, self-employed individuals, and nonprofits (including churches).

As with the first round of PPP loans, 60% of the funds must be spent on payroll over the covered period (8 or 24 weeks).

Other provisions affecting businesses

$13.5 billion for Economic Injury Disaster Loans (EIDLs)

$15 billion in grants for theaters and live venues – Theaters and live venues must have been operational prior to Feb. 29, 2020, have at least a 25% reduction in gross revenue, and they plan to resume operations following closures. Grants can be up to $10 million per eligible business, with preference given to venues with higher revenue losses. Certain characteristics apply for live venue spaces, movie theaters, and museums, so work with your CPA to determine eligibility.

Employer tax credits for those offering paid sick leave have been extended to Mar. 31, 2021, for employers who voluntarily choose to expand paid emergency leave. Otherwise, the requirements set forth by the Families First Coronavirus Response Act (FFCRA) expire Dec. 31, 2020.

Extension of time for employers to payback deferred payroll taxes till the end of 2021 instead of Apr. 30, 2021.

$10 billion for childcare assistance – This includes supplemental assistance for childcare providers to assist with fixed costs and operating expenses.

Provisions affecting individuals

Direct stimulus payment of $600 per adult and child with the same phase out thresholds as the CARES Act ($150,000 if married filing a joint return, $112,500 if filing as head of household, or $75,000 for individuals). Payments are expected to start arriving as early as the week of Dec. 28, 2020.

Changes and extensions to unemployment including:

$300 in enhanced unemployment benefits for unemployment beginning after Dec. 26, 2020, through Mar. 14, 2021, fully financed by the federal government, instead of split between the states and federal government.

Extension of the Pandemic Unemployment Assistance program for gig workers, independent contractors, and the self-employed.

Extension of the Pandemic Emergency Unemployment Compensation program which protects workers who exhaust state benefits with an additional 13 weeks.

$25 billion for rental assistance.

An extension of the eviction moratorium through Jan. 31, 2021.

$13 billion for enhanced Supplemental Nutrition Assistance Program (SNAP) benefitsincluding funding a 15% increase in benefits for 6 months to recipients.

Other provisions

$81.8 billion allocated to colleges and schools to assist with pandemic-related changes in operations.

$45 billion for transportation including $2 billion for airports and $15 billion for passenger airline workers.

$7 billion for increased broadband access to assist with remote business operations and learning.

$28 billion in funding for vaccine purchase and distribution.

$22 billion for state, local, tribal, and territorial governments for health-related expenses like testing.

Further guidance and regulations are expected in various components of the bill and are due in periods of 10 to 45 days depending on the issue and reporting agency. Not included in the bill was aid for state and local governments, an agreement on liability protections for businesses, nor a continued freeze on payments and interest for federal student loans set to expire for many in February. Lawmakers have indicated they expect to pass another stimulus bill addressing some of these issues in early 2021.

More guidance and updates are expected on the Coronavirus Response & Relief Supplemental Appropriations Act. Stay tuned for more details in the days and weeks to come.

Please note that information and guidance on the PPP loan program is changing on a daily basis. The information provided in this article is current as of December 22, 2020. It is intended for general informational purposes only. Consult with your financial advisor about your specific situation.

The pandemic created by the novel coronavirus has drastically changed the way we live and work. As more businesses are forced to send their employees home, work-from-home life has become a mainstay especially in knowledge-based jobs (jobs that do not require physical labor), and many of these industries are not going back to the workplace anytime soon. This can create wrinkles for both employers and employees when it comes to their tax situations.

Here’s what employers and employees need to know about remote work and the impact it can have on taxes.

Tax and labor considerations for employers with remote employees

Nexus – Employers who have transitioned their workforce to be remote must be conscious of potential nexus implications due to any employees now working from another state. Working out of state from the employer can create physical nexus which means the employer will be responsible for the taxes imposed from the employee’s location. This could include taxes on income, gross receipts, and sales and use from both the city and county level.

Some states have waived these nexus rules or have adjusted in light of COVID-19 including Minnesota, Indiana, Ohio, New Jersey, Mississippi, Pennsylvania, North Dakota, and the District of Columbia. Check with your CPA to ensure you’re following your state’s remote worker nexus law.

Labor and employment law – Changes in an employee’s location across state lines can result in new wage and hour rules, termination of employment considerations, noncompetition agreements, trade secrets protections, and paid sick and family leave rules. Employers will want to be mindful of worker’s compensation insurance as states usually require employers to register and obtain premiums to cover the employee in that state. Additionally, unemployment insurance is also required by states for employees even if the employer operates in a different state.

Remote worker supplies – Employers who purchased items and provided them to workers in order to move operations remotely may deduct those expenses on their tax return. As these supplies are usually purchased for non-compensatory business reasons, employees do not need to pay taxes on them. Employers who reimbursed employees for purchased supplies deemed “ordinary and necessary” should have accountability plans and policies in place to protect the employee from taxation.

Consistent and accurate communication with employees during this time is key in order to avoid employer and employee tax violations as tax updates continue to be released regarding nexus and tax responsibilities. Be mindful that employee tax obligations are not the employer’s responsibility, so remind your employees to stay vigilant about their personal tax situation.

Tax implications for employees working from home

Double-taxation – Double-taxation can be a large burden for employees living in one state and working in another. Double-taxation occurs when the resident state doesn’t provide and employee with a credit on their return for taxes paid to their employer’s state. States where this can occur include New York, Arkansas, Connecticut, Delaware, Nebraska, and Pennsylvania.

Home office deductions – The Tax Cuts and Jobs Act (TCJA) of 2017 removed the itemized home office deduction for unreimbursed expenses exceeding 2% of AGI. This means that even though new remote employees have had to procure supplies during the pandemic and they were not either directly purchased by the employer or the employee was not reimbursed, those expenses are not tax-deductible.

Self-employed individuals are still eligible for the home office deduction if they are purchasing their own supplies. If a contracting client purchases supplies for them, those would be tax-deductible for the client, but not the self-employed individual.

Relocation – If you’ve permanently relocated across state lines during the pandemic, you will need to file tax returns for both states in 2021. Even temporary relocations of six months or longer may require tax returns to be filed in two states. It is likely states will be monitoring these moves closely in order to recover lost revenue.

Employers who have never operated with remote workers prior to the pandemic could face significant headaches come tax time. Likewise, employees who are working in one state and living in another could face large tax bills in 2021. For assistance with your obligations as an employer or individual taxpayer, reach out to us.

On November 18, 2020, the Internal Revenue Service issuedRevenue Ruling 2020-27 which provides needed clarity on a taxpayers’ ability to deduct eligible expenses for Paycheck Protection Program (PPP) loan forgiveness.

The Ruling notes that a taxpayer that received a covered loan guaranteed under the PPP and paid or incurred certain otherwise deductible expenses listed in section 1106(b) of the CARES Act may not deduct those expenses in the taxable year in which the expenses were paid or incurred if, at the end of such taxable year, the taxpayer reasonably expects to receive forgiveness of the covered loan on the basis of the expenses it paid or accrued during the covered period, even if the taxpayer has not submitted an application for forgiveness of the covered loan by the end of such taxable year.

What if forgiveness is denied, in whole or part, or not requested?

In conjunction with the Ruling, the IRS issuedRevenue Procedure 2020-51 to outline the steps for when:

1.) The eligible expenses are paid or incurred during the taxpayer’s 2020 taxable year,

2.) The taxpayer receives a covered loan guaranteed under the PPP, which at the end of the taxpayer’s 2020 taxable year the taxpayer expects to be forgiven in a subsequent taxable year, and

3.) In a subsequent taxable year, the taxpayer’s request for forgiveness of the covered loan is denied, in whole or in part, or the taxpayer decides never to request forgiveness of the covered loan.

The Rev Procedure provides for two safe harbors for taxpayers in the event forgiveness is denied, in whole or in part, or otherwise not requested that would allow for the deduction of expenses in either the 2020 or a subsequent tax year.

Questions we still have

While the Ruling provides information on the deductibility of expenses and the tactical approach for borrowers whose forgiveness is denied or not requested, additional clarification is still needed. This guidance does not address the order in which the eligible expenses (payroll, rent, utilities and mortgage interest) lose the ability to be deducted.

Further, the guidance does not address other matters that could have significant tax implications including, but not limited to, the impact on the following:

Qualified business income deduction (Section 199A)

Research and development credits

Interest deduction limitation (Section 163(j))

Need Assistance in Choosing the Right PPP Loan Forgiveness Application?

This year has been unique and beyond comparison in many ways, and tax planning is just one of the implications of current events. Both individual and business taxes have the potential to be significantly impacted by the various legislation that has passed like the FFCRA and the CARES Act, the loan programs made available like the PPP and the EIDL, and the unemployment/stimulus programs that touched many Americans.

It’s imperative that we take into account all these potential factors when implementing your tax plan for 2020. In this article, we’lltake a look at the main areas to consider, both common and pandemic-related, when planning for 2020 year-end taxes.

Common and pandemic-related tax planning items for businesses to consider in 2020

Accelerate AMT refunds – The CARES Act has accelerated the alternative minimum tax following changes made by the Tax Cuts & Jobs Act. Corporations can claim all remaining credits in 2018 or 2019 thus allowing for filing of quick refunds.

Use current losses for quick refunds – The CARES Act allows businesses to claim immediate refunds by using current losses against past income, for example.

Submit a retroactive refund for bonus depreciation – Businesses can now deduct qualified improvements dating back to Jan. 1, 2018, thanks to a fix made by the CARES Act. This could offer a quick refund.

Claim quick disaster loss refunds – Nearly every U.S. business is eligible for disaster-related refunds from losses in 2020 on an amended 2019 return for a quicker refund.

Time out your payroll tax deduction – While the CARES Act allows employers to defer paying their share of Social Security taxes, you should review the best strategy with your accountant. In some cases, it’s better to pay on time to take a loss. In others, it provides a liquidity benefit.

Maximize generous Section 179 deduction rules – For qualifying property placed in service in tax years beginning in 2020, the maximum Section 179 deduction is $1.04 million. The Section 179 deduction phase-out threshold amount is $2.59 million.

Understand your PPP obligations – PPP loan forgiveness may be excluded from gross income, but how to treat expenses related to PPP loans is still in question. Does the taxability of these expenses come into play in 2020, or not until 2021 when a loan is forgiven? This can impact estimated tax payments and how to treat nondeductible expenses once a decision is made.

Deduct EIDL grant expenses – EIDL grant funds are believed at this point to be considered taxable income but expenses related to this grant would be deductible.

Claim any employment retention tax credits – These can be claimed now, but you cannot have a PPP loan and receive employment retention credits.

Common and pandemic-relatedtax planning items for individuals to consider in 2020

Be mindful of long-term capital gain taxes from sales of assets as these could also impact the 3.8% tax on net investment income.If you didn’t make much income in 2020, consider harvesting some long-term gains, especially if you qualify for the 0% capital gains tax bracket (under $80,000 MFJ, $40,000 single filer).

Postponeincome and acceleratedeductions – Check on the status of your current and projected income for 2020 and 2021 to see if you’ll be pushed into a higher tax bracket. Defer bonuses from employers if necessary, and if self-employed, postpone income by postponing billing. It may also be possible that accelerating income is the appropriate path for you to lock in lower tax rates.

Convert traditional IRAs to Roth IRAs – Be mindful of the new distribution rules for IRA beneficiaries as well as the ability to continue to make IRA contributions after age 70½ if there is enough earned income at play.

Bunch deductions if necessary/appropriate –Consider bunching charitable contributions (by using a donor advised fund or charitable lead trust) and medical deductions as there are certain thresholds only available for 2020. Thirty regularly expiring provisions are also coming with 2020 including tuition/fees deduction and mortgage insurance premium deduction among others.

Make your year-end gifts as interest rates are low (expected to continue in 2021).

Account for your stimulus payment – Stimulus payments are considered an advance on your 2020 tax credit, so you may see a smaller return next year.

Pay taxes now on your unemployment income – Unemployment benefits are taxable on the federal level so ensure you’re taking these taxes out of your payments or saving to make a payment. Note that states have varying tax treatment of unemployment income.

Consider taking gains and paying more in tax now if you’re in a good financial position – This is contrary to the usual advice, however given our current historically low rates and a large and accelerating national debt, higher tax rates seem inevitable. For example, paying a 20% LTCG tax now could be very advantageous for a high–income filer who might be stuck paying at their ordinary rates on capital gains in the future.

Exercise non-qualified stock options – Biden has proposed not only a rate increase, but also a FICA increase on high income taxpayers. So, corporate executives might consider exercising the NQSOs now to avoid getting hit with higher rate and FICA in the future.

As mentioned in our previous article – Tax planning considerations: Election results, sunset provisions – changesto the tax code in the next two to four years may still be imminent depending on the finalizations of certain Senate elections. If those changes become a likely scenario, someadjustments may still be possible in this year’s tax plan to account for those potential tax code changes. Work with your CPA to have a plan for all scenarios.

According to news outlets, as of this writing, Joe Biden will be the president-elect of the U.S. following the Electoral College vote on Dec. 14. Vote counting is still ongoing and election results have not yet been certified, but this news may have some taxpayers wondering what changes, if any, they should make in their tax planning to close out an eventful tax year.

The likelihood of a major tax overhaul in the next two years is up in the air as the Senate is not yet decided and may not be until two Georgia run-off elections in January 2021. If Republicans retainthe majority, it’slikely therewon’t be many changes, but that doesn’tcompletely lock out any potential adjustments that could come in the next two to four years. Items of agreement on tax policy exist between both parties such as increasing the child tax credit. However, with provisions of the Tax Cuts and Jobs Act (TCJA) set to sunset in 2026, updates to the tax code will be on the horizon by the next election.

Additionally, if the Republican Party indeed holds onto a 51-vote majority in the Senate, it is not unreasonable to imagine a legislative vote in which 2 republican senators vote against the majority of the Republican party to push a tax legislation bill through to the President. Accordingly, between the possibility of a loss of Republican control in 2 to 4 years, the possibility of 2 Republicans voting for a tax reform bill, and the 2026 TCJA sunset, it is highly unlikely tax laws will become more favorable to taxpayers in the in future; thus, we believe there is an urgency to plan carefully and diligently in the last weeks of 2020.

In this article, we’ll examine the key points of the President-elect‘s tax plan, the sunsetting TCJA provisions, and what to keep in mind as you execute your tax plan to close out the year.

High-level overview of the President-elect Biden’s tax plan

President-elect Biden has laid out several of his tax plans the past year on the campaign trail. Here’s what we know based on what he’s shared.

For individuals:

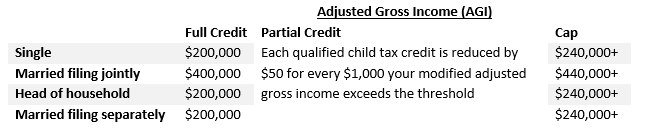

Increase the top tax rate on ordinary income for individuals with taxable income over $400,000 to 39.6%

Tax long-term capital gains at ordinary income rates for those with taxable income over $1 million

Cap the value of itemized deductions at 28% for those with incomes over $400,000

Increase the child tax credit to $3,000 for children 6-17 years of age, and increase to $3,600 for children under age 6, make credit fully refundable

Increase tax preferences for contributions to 401(k) plans and IRAs for middle-income taxpayers

Replace deduction with a refundable tax credit for worker contributions to traditional IRAs and defined-contribution pensions

Increase tax benefits for the purchase of long-term care insurance using retirement savings for older Americans

Raise eligibility limits on health care premium tax credits and increase the amount of the credit

Repeal the per-manufacturer cap on electric vehicle tax credits, make credit permanent, phase out credit for those with income above $250,000

Reinstate solar investment credit and tax credits for energy efficiency in residences

For businesses:

Phase out the qualified business income (QBI) deduction for those with income greater than $400,000

Expand Social Security taxby increasing the maximum threshold from $137,000 to $400,000 over time

Increase the corporate tax rate to 28%

Add a 15% minimum tax on “book” income

Offer tax credits to offset costs of workplace retirement plans for small businesses

Establish a refundable tax credit for companies and nonprofits who provide full health benefits to all workers during a period of work hour reductions

Eliminate certain tax subsidies for oil, gas, and coal production, enhance tax incentives for carbon capture use and storage, establish tax credits and subsidies for low-carbon manufacturing

Expand tax deductions for commercial buildings with certain environmentally friendly investments

TCJA provisions to sunset in 2026

In addition to the President-elect’s plans, the TCJA is still in the spotlight. The TCJA was the most significant tax overhaul in decades when it was passed in 2017. However, as is the nature when dealing with budgetary constraints, many of the provisions of the TJCA are scheduled to sunset by 2026. Below we’ve highlighted a few of the anticipated changes.

For businesses, approximately $4 trillion is expected in new taxes over the next 10 years as provisions begin to sunset including changes to:

Alternative Minimum Tax (AMT)

Elimination or scale back of Section 199

Capital gains

Payroll taxes

Bonus depreciation

For individuals, changes are coming for:

Marginal tax rates for upper-income taxpayers

Caps on itemized deductions

Wealth taxes

Childcare/family caregiving

Renter’s credits/first-time homeowner credit

Considerations for 2020 year-end tax planning

It’s important to note that the above considerations are not an exhaustive list of tax items to review as we close 2020. Work with us to have a proactive plan in place that takes into account various potential scenarios that could manifest in the coming weeks and months. In our follow-up article – 2020tax planning considerations for businesses, individuals – we’ve laid out some of the key provisions to take into account as you work with uson your end–of–year tax planning.

With all of the curveballs 2020 has thrown at the nation, the economy, and businesses, there’s never been a better time to get an early jump on year-end planning for your business. While all the usual year-end tasks are still on the docket, you’ll want to consider implications related to the Paycheck Protection Program (PPP), any disaster loan assistance you received, and changes made by the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

We’ve put together a checklist of what you need to do now to prepare for a great year-end that includes annual tasks as well as 2020-specific tasks. Keep reading for assistance getting your financials organized, reviewing your tax strategy, and preparing for next year.

Get organized

1. Bring order to your books – Now is the time to collect, organize, and file all ofyour receipts for the year if you haven’t been staying on top of it. Get with your CPA to ensure everything is clean and in order before the end of the year to help avoid surprises come tax time.

2. Examine your finances – This includes having your balance sheet, income statement, and cash-flow statements prepared and up to date. Reviewing this information allows you to see where your money went for the year so you can properly prepare for next year.

3. Work with your CPA on your PPP loan forgiveness application – We are currently awaiting further guidance on the PPP’s impact to taxes, but it’s important to work with your CPA on your PPP loan forgiveness application. Knowing where your PPP loan lies can help determine how to spread out your cash flow for the remainder of the year.

4. Organize all disaster loan assistance documentation – This includes your Economic Injury Disaster Loan (EIDL) documentation if you received an advance grant. EIDL advances must be added to your taxable income (unless different guidance is released), but you’ll be able to deduct any expenses paid with this grant.

Review your tax strategy

5. Review your taxes with your CPA – Do not put off your tax planning meeting with your CPA. Especially after the year you’ve had and any potential federal state aid your business received, your tax plan needs a review. Getting a jump on this early, well before the new year, can help you plan for what’s to come on Tax Day. It’s even more imperative to plan early for any tax obligations you may have at tax time as it’s likely the COVID-19 pandemic will continue to create a volatile environment for many industries’ revenue projections.

6. Execute on year-end tax strategy adjustments such as:

Accelerating AMT refunds – The CARES Act has accelerated the alternative minimum tax following changes made by the Tax Cuts & Jobs Act. Corporations can claim all remaining credits in 2018 or 2019 thus allowing for filing of quick refunds.

Using current losses for quick refunds – The CARES Act allows businesses to claim immediate refunds by using current losses against past income, for example.

Submitting a retroactive refund for bonus depreciation – Businesses can now deduct qualified improvements dating back to Jan. 1, 2018, thanks to a fix made by the CARES Act. This could offer a quick refund.

Claiming quick disaster loss refunds–Nearly every U.S. business is eligible for disaster-related refunds from losses in 2020 on an amended 2019 return for a quicker refund.

Timing out your payroll tax deduction – While the CARES Act allows employers to defer paying their share of Social Security taxes, you should review the best strategy with your accountant. In some cases, it’s better to pay on time to take a loss. In others, it provides a liquidity benefit.

Cash in on generous Section 179 deduction rules – For qualifying property placed in service in tax years beginning in 2020, the maximum Section 179 deduction is $1.04 million. The Section 179 deduction phase-out threshold amount is $2.59 million.

7. Prepare your tax documents – Once you’ve met with your CPA, it’s time to line up all the info you need to prepare your final tax documents or have your CPA take care of it. Be sure not to put this off to the last minute as it will be a complicated year for everyone.

8. Automate your tax function – Instead of spending valuable time and energy on manual tasks and repetitive processes this year, consider investing in data analytics and automation tools to optimize and streamline your in-house accounting and tax functions. There’s never been a better time to invest in technology that will help you become more efficient and accurate.

Plan for the future

9. Evaluate your goals – There’s no doubt that 2020 likely threw a wrench in many of your goals for the year. However, you should still review the goals you set last year and see if you’ve met or made progress on any of them. This will help with 2021 business planning.

10. Set goals for the new year – No one knows how 2021 will play out, and it’s unlikely the market or business will return to normal in the first part of the year. Take into consideration the challenges you’ve faced so far in the pandemic as you plan for 2021. Work with your trusted advisor to determine several back-up plans for what if scenarios in case of any state or national lockdowns.

In a year like no other, it’s crucial to prepare like no other so you’re not met with any surprises or devastating fees. Contact us today to set up your tax and business planning appointment.

The Tax Cuts & Jobs Act (TCJA) of 2017 made many significant changes for business tax deductions including the disallowing of the business deductions for most entertainment expenses. After a period of comments and proposed regulations, the IRS has released long-awaited final regulations for the treatment of meals and entertainment deductions, and businesses should apprise themselves of these changes.

The main change with the TCJA was the removal of certain entertainment expenses as tax deductible for a business. Prior to the TCJA, entertainment expenses were eligible for an up to 50% deduction in expenses directly related to the active conduct of a trade or business or for expenses incurred before or after a bona fide business discussion. The TCJA eliminated this deduction for activities considered to be entertainment, amusement, or recreation as well as removed the reference to entertainment as part of the 50% limitation of deductibility for food or beverages.

The final rules clarify that taxpayers may continue to deduct 50% of business meals if the taxpayer or an employee of the taxpayer is present, as long as the meal is not considered extravagant. Meals for current or potential business customers, clients, consultants, or similar business contacts are eligible. Food and beverages provided during entertainment events must be purchased separately from the event to qualify, otherwise they are considered part of the entertainment.

Note that the TCJA did not repeal the exception for certain recreational activities that benefit employees, reimbursed expenses, entertainment treated as employee compensation, or includable gross income of a nonemployee as compensation or as a prize or award, which must be properly reported by the taxpayer.

Separating meals and entertainment and aligning them in the right buckets for deduction can be tricky. Contact us for assistance in determining what qualifies.

If a relative needs financial help, offering an intrafamily loan might seem like a good idea because they allow you to take advantage of low interest rates for wealth transfer purposes. But if not properly executed, such loans can carry negative tax consequences — such as unexpected taxable income, gift tax or both. Here are five tips to help avoid any unwelcome tax surprises:

1. Create a paper trail. In general, to avoid undesirable tax consequences, you need to be able to show that the loan was bona fide. To do so, document evidence of:

The amount and terms of the debt,

Interest charged,

Fixed repayment schedules,

Collateral,

Demands for repayment, and

The borrower’s solvency at the time of the loan.

Be sure to make your intentions clear — and help avoid loan-related misunderstandings — by also documenting the loan payments received.

2. Demonstrate an intention to collect. Even if you think you may eventually forgive the loan, ensure the borrower makes at least a few payments. By having some repayment history, you’ll make it harder for the IRS to argue that the loan was really an outright gift. And if a would-be borrower has no realistic chance of repaying a loan, don’t make it. If you’re audited, the IRS is sure to treat such a loan as a gift.

3. Charge interest if the loan exceeds $10,000. If you lend more than $10,000 to a relative, charge at least the applicable federal interest rate (AFR). Be aware that interest on the loan will be taxable income to you. If no or below-AFR interest is charged, taxable interest is calculated under the complicated below-market-rate loan rules. In addition, all of the forgone interest over the term of the loan may have to be treated as a gift in the year the loan is made. This will increase your chances of having to use some of your lifetime exemption.

4. Use the annual gift tax exclusion. If you want to, say, help your daughter buy a house but don’t want to use up any of your lifetime gift and estate tax exemption, you can make the loan and charge interest and then forgive the interest, the principal payments or both each year under the annual gift tax exclusion. For 2020, you can forgive up to $15,000 per borrower ($30,000 if your spouse joins in the gift) without paying gift taxes or using any of your lifetime exemption. But you will still have interest income in the year of forgiveness.

Here is an example of how an intrafamily loan can save on taxes:

A $2 million interest-only loan is made from parent to child at an interest rate of 0.38%. If the loan proceeds are invested and grow at a rate of 5%, after repayment of interest and principal in year 5, the child is left with approximately $510,000 estate and gift tax-free. This arrangement also offers the flexibility to utilize the gift tax exemption at any time.

5. Forgive or file suit. If an intrafamily loan that you intended to collect is in default, don’t let it sit too long. To prove this was a legitimate loan that soured, you’ll need to take appropriate legal steps toward collection. If you know you’ll never collect and don’t want to file suit, begin forgiving the loan using the annual gift tax exclusion, if possible.

The unprecedented global pandemic and record unemployment has resulted in a dramatic drop in interest rates. Many people focus on the Fed rate and mortgage rates, and rightfully so, but for some, the focal point should be on the historically low IRS interest rates.

The IRS posts various interest rates, generally on a monthly basis. The Applicable Federal Rate (“AFR”) and the Internal Revenue Code Section 7520 Rate (“7520 Rate”) are among the most important. Many tax strategies are a function of calculations driven by the AFR and 7520 rates. Some strategies work best in high rate environments while other work best in low rate environments. Accordingly, any time the IRS rates dramatically rise or fall, we should take notice and consider tax planning.

The May 2020 IRS Rates include:

Short-Term AFR: 0.25%

Mid-Term AFR: 0.58%

Long-Term AFR: 1.15%

7520 Rate: 0.80%

These rates are exceptionally low. To provide some context for comparison, the May 2019 Rates were: Short-Term AFR 2.39%, Mid-Term AFR 2.37%, and Long Term AFR 2.74%. Viewing this from a historical perspective, the May 2019 rates were low in their own right, but clearly the rates today, just one year later, are materially lower.

The remainder of this paper outlines three strategies that work particularly well in low interest rate environments. Although we have elected to highlight three strategies specifically, low interest rate tax strategies are not limited to just these three. Accordingly, we encourage you to contact our office to discuss your specific set of circumstances.

Charitable Lead Trusts

A Charitable Lead Trust (“CLT”) is a split interest trust, meaning there are two categories of beneficiaries: (1) a current beneficiary and (2) a remainder beneficiary. The current beneficiary receives distributions from the CLT for a period of time (the “Term”) and must be a charitable organization, such as a public charity, a church, most schools and universities, and even a private foundation operated by the donor. The remainder beneficiary receives all the assets remaining in the CLT after the Term expires and is generally the donor or the donor’s children. Depending on the design of the CLT, the donor may receive an income tax deduction in the tax year the CLT is established in an amount equal to the present value of all payments that will go to charity during the CLT’s term. Accordingly, it can generate a substantial income tax deduction for gifts that have not yet gone to the charity. This gives the donor the ability to continue investing and growing the CLT assets, thereby ultimately benefiting the donor who will receive the assets back upon expiration of the CLT term.

Why CLTs during low interest rates?

The donor’s income tax deduction is a present-value calculation. We take the sum of all scheduled future charitable distributions and discount that number to present value using a calculation based on the 7520 Rate. The lower the 7520 Rate, the lower the discount. The lower the discount, the greater the deduction. Accordingly, in today’s environment, all other factors being exactly the same (i.e. same growth rate, same amount to charity, etc.), a CLT today will generate a significantly higher income tax deduction, than the same CLT when interest rates are higher.

Grantor Retained Annuity Trusts

Grantor Retained Annuity Trusts (“GRATs”) are estate planning trusts that provide a tremendous opportunity to transfer wealth from one generation (“Generation 1”) to the next (“Generation 2”), often without incurring gift or estate taxes. GRATs are established with Generation 1 assets for a period of time (the “Term”). During the Term, the GRAT makes distributions to Generation 1. At the end of the Term, if designed properly, the assets remaining in the GRAT transfer to Generation 2 free of gift, estate, or transfer taxes. Many individuals will establish a series of GRATs in order to provide necessary lifetime cash flow to Generation 1.

Why GRATs during low interest rates?

Payments made from the GRAT to Generation 1 are based on the IRS rates. The donor makes the “bet” that the assets inside the GRAT will grow at a rate higher than the IRS rates. Lower rates mean a lower hurdle, a lower hurdle means more wealth can transfer to Generation 2 tax-free.

Sales to Intentionally Defective Grantor Trusts

Intentionally Defective Grantor Trusts (“IDGTs”), are irrevocable estate planning trusts that are generally utilized by high net worth business owners and those with assets likely to significantly increase in value (such as stock and real estate). The IDGT will purchase the asset from the individual primarily in exchange for a promissory note (there are no income taxes due on the sale because the IDGT is disregarded for income tax purposes). The IDGT will make installment payments to the individual for the term of the promissory note. The assets in the IDGT are outside of the individual’s estate, therefore any growth in the asset from the time it is sold remains outside of the individual’s estate for estate tax purposes.

Why IDGTs during low interest rates?

Similar to any traditional lending arrangement, the IDGT promissory note must yield interest. Because this is a related-party transaction, the IRS mandates a certain minimum interest rate, which is based on the AFR. The lower the AFR, the lower the required monthly payments, and thus more taxable wealth remains outside of the Grantor’s estate.

Next Steps?

Don’t let this exceptionally low interest rate environment get away. Please contact your Heritage financial advisor, CPA, or attorney to schedule a planning session.

This article has been edited by Hamilton Tharp LLP. This article originally appeared on the HWM newsletter.

As consumers become more conscious of their environmental footprint, and look for ways to save money, more and more electric vehicles can be seen on the roads today stretching from coast to coast. At this point, most taxpayers know or have heard of an electric vehicle tax credit program, but what they may not know is that there are specific conditions and limitations that must be met, and that some vehicles have actually phased out of the program. So, before you consider an electric vehicle for your next purchase, make sure it qualifies.

Here’s a rundown of what you need to know about the electric vehicle tax credit, how it works, and what qualifies.

What vehicles qualify for the electric vehicle tax credit?

The new car or truck must:

· Have at least four wheels and gross vehicle weight of less than 14,000 pounds

· Draw energy from a battery with at least 4 kWh hours and recharged from an external source

· Purchased after 2010 and begun driving in the year claiming the credit

· Be primarily used in the U.S.

Two or three-wheeled vehicles purchased in 2012 or 2013 and used within that year may qualify under section 30D(g) if they draw from a battery with at least 25 kWh and charged from an external source.

How much is the electric vehicle tax credit?

The tax credit for an electric vehicle can range from $2,500 to $7,500 depending on the vehicle with higher credit amounts for specific battery capacities and vehicle sizes. For two or three-wheeled vehicles, the credit is 10% of the purchase price up to $2,500.

How is the tax credit applied to me?

The non-refundable tax credit is filed on your federal tax return (for individuals on your 1040), and your liability determines how much credit you qualify for. The non-refundable caveat means that in order to receive the full $7,500 credit, your tax liability must be at least that much. If your liability is only $3,000, you’ll only receive $3,000. You won’t receive the difference in a refund check.

Can I get a tax credit on a used or leased vehicle?

Unfortunately, the answer is no to both of those circumstances. The credit only applies to the new purchase and the person who actually owns it. Used vehicle purchases, even transfers to family members don’t qualify, and if you lease, the credit actually goes to the manufacturer

offering the lease. Some manufacturer dealers offer lower prices on leased electric vehicles as a result of the incentive, but are not forced to do so.

Does the tax credit run out?

As sales of electric vehicles increase, the tax credit will phase out. Once a manufacturer reaches 200,000 qualified vehicles, the credit begins to phase out with a step-down process over the course of a year. No tax credits are available for Tesla vehicles sold after Dec. 31, 2019, as they hit their mark in July 2018, and no credits are available for GM vehicles after March 31, 2020, as they hit their mark as well. You can see a list of the vehicles available for credits at fueleconomy.gov.

Are there state tax credits available?

Some states and regions do offer tax credits for electric vehicles and alternative-fuel vehicles, but these often apply to businesses. Individuals may receive incentives such as carpool lane access or free parking. Some states offer rebates for retail buyers. The U.S. Department of Energy offers a chart of state incentives.

For Californians, a $2,000 or $1,000 rebate is available depending on which type of electric car you purchase. Fully electric cards usually receive the higher rebate with hybrids on the lower end. Hydrogen fuel vehicles are eligible for a $4,500 rebate in California. These rebates are in addition to the federal tax credit and can reduce the out of pocket cost for a car by close to $10,000. You can learn more about California’s Clean Vehicle Rebate Project on their website.

For assistance with the electric vehicle tax credit and determining any extra state or local incentives, reach out to us.

Employers can now defer payroll tax withholding on employee compensation for the last four months of 2020 and then withhold the deferred amounts in the first four months of 2021, confirms a recent update from the IRS. President Trump’s memorandum on Aug. 8 gave employers the ability to defer payroll taxes for employees affected by the COVID-19 pandemic in an effort to provide financial relief.

The guidance directs that employers can defer the withholding, deposit, and payment of the employee portion of the old-age, survivors, and disability insurance (OASDI) tax under Sec. 3102(a) and Railroad Retirement Act Tier 1 under Sec. 3201 from employee wages from Sept. 1 to Dec. 31, 2020.

Employers must then withhold and pay the deferred taxes from wages and compensation during the period from Jan. 1, 2021, and April 30, 2021, with interest, penalties, and additions to tax to begin accruing starting May 1, 2021. Included in the notice is a line that indicates, if necessary, employers can “make arrangements to otherwise collect the total Applicable Taxes from the employee,” such as if an employee leaves the company before the end of April 2021, but does not provide details on what that entails.

Employees with pretax wages or compensation during any biweekly pay period totally less than $4,000 qualify for the deferral. Amounts normally excluded from wages or compensation under Secs. 3121(a) or 3231(e) are not included in calculating the applicable wages. The determination of applicable wages should be made on a period-by-period basis.

Companies may choose whether or not to enact the payroll tax deferral. We are closely monitoring updates related this and other presidential executive orders and will communicate if more information becomes available. For questions or assistance with this payroll tax deferral, contact us.

In an effort to help businesses cope with the impact of COVID-19, the CARES Act passed by Congress in March of this year eliminated some of the restrictions on the business interest deduction set in place in 2017 by the Tax Cuts and Jobs Act (TCJA). Now, the IRS has released much-needed guidance and final regulations for business interest expense deductions.

Limiting the business interest deduction was originally a way of helping pay for the TCJA and began with tax years starting after Dec. 31, 2017. The deduction was limited to the sum of:

The taxpayer’s business interest income

30% (or 50% if applicable) of the taxpayer’s adjusted taxable income, and

the taxpayer’s floor plan financing interest expense

The final regulations state that the deduction does not apply to:

Certain small businesses with gross receipts of $26 million or less (applies to 2020 tax year, adjusted annually for inflation)

Electing real property trades or businesses (cannot claim additional first-year depreciation deduction on certain types of property held)

Electing farming businesses (cannot claim additional first-year depreciation deduction on certain types of property held)

Certain regulated public utilities

Taxpayers must use Form 8990 to calculate and report their deduction and the carry-forward amount of disallowed business interest expense.

Additional regulations released by the IRS cleared up some of the remaining questions including issues related to the CARES Act. These additional regulations can be used with limitations until the final regulations are published in the Federal Register.

Additionally, a safe harbor was created in Notice 2020-59 that allows taxpayers engaged in a trade or a business managing or operating qualified residential living facilities to treat that as a real property trade or businesses in order to qualify as an electing real property trade or business.

Reach out for assistance with understanding and reporting your business interest expense.

Economic downturns are an almost inevitable reality for nearly every business owner. Decisions made far away from your community, catastrophic and unpredictable weather events, and even global pandemics as we’ve seen this year can disrupt the health and viability of a business. During these challenging times, business owners have to make difficult decisions about the future of their business that not only affect them but also their employees, vendors, clients, and communities. It’s an enormous responsibility to bear, but you don’t have to go it alone.

Your CPA advisor is your best resource for tackling the challenges of an economic downturn. As an outside party, they can help you make smart business decisions that protect your vision and mission while remaining financially responsible. Your CPA can help you:

Optimize your books

Never underestimate the power of good bookkeeping. By keeping your books in order, your CPA can help you plan and project for the future at each stage of an economic downturn. This includes planning for temporary closures and tiered re-openings (and potentially a back-and-forth of both depending on the state of the country and market). When your books are clean and up to date, you can better project how events and decisions will impact your finances on a weekly, monthly, and quarterly basis. Your CPA can help you flex the numbers on fixed and variable expenses to account for increases in costs, decreases in income, and potential changes to payroll. Knowing your numbers intimately can help you make better-informed decisions.

Minimize your tax burden

During times of economic crisis, staying abreast of new and changing tax legislation will be essential to projecting tax burden and uncovering tax savings opportunities. Your CPA is the best person to handle this because they know your business and your industry inside and out and can help you uncover tax savings opportunities that are unique to your circumstances. They do all the research, and you reap the rewards. With a CPA’s assistance, you achieve deductions and credits you may not have realized were available and develop a plan to defer costs where allowed depending on your business, industry, and location. Taxes are not an area you should or need to face alone during an economic downturn. Your CPA has done the homework, so you don’t have to.

Rationalize your decision making

When markets are in flux and your business is facing unprecedented challenges, the decisions you make can make or break your business. But you don’t have to go it alone. Your accountant can help you make data-informed decisions whether that be how to pay vendors, when and how to apply lines of credit, and the best ways to use your capital. Negotiating contracts with vendors that meet your needs and theirs during a downturn will not only achieve cost savings but also preserve relationships – your CPA can help develop a plan that makes sense. Knowing when to engage lines of credit can help you make better moves that you can either afford to pay back later, or maybe prevent you from taking on credit you can’t handle – your CPA can guide you in this process. Knowing where to allocate capital will be key to maintaining operations, and you may need guidance on what expenses to cut and what to keep such as marketing and payroll – your CPA can help you project the ramifications. With your CPA by your side, you don’t have to operate in a silo of decision-making.

Maximize your sense of relief

Most of all, your CPA can provide perspective, alleviate business back-end burden, and help advise you on financially feasible and sound decisions when much of the world feels like it’s in chaos. You have a lot to focus on during a downturn including how to handle your customers and employees in a changing marketplace. Having someone who can help you stay fiscally viable as you work through tough times, and develop a plan for future success, provides a welcome peace of mind.

You don’t have to go through any economic downturn alone. Your CPA can help you shoulder the challenges and weather the storms so you can continue doing what you do best – running your business.

In the midst of the uncertainty and instability that the COVID-19 pandemic has created for businesses and individuals, some relief is available for taxpayers in the form of deductible losses thanks to the preexisting Internal Revenue Code (IRC) Section 165(i). While the CARES Act and FFCRA have received much of the attention, taxpayers may also find relief thanks to Section 165(i) which allows for losses sustained as a result of the pandemic in 2020 to be claimed on the taxpayer’s 2019 tax return.

This deduction is triggered by a federally declared disaster, like the pandemic which was declared a national emergency on March 13, 2020. In the case of this deduction, losses attributed to federally declared disasters can be deducted on the previous year’s return. While not often used, this deduction comes at the right time for businesses struggling during the pandemic.

In order to claim the Section 165(i) deduction, losses must:

Be attributable to a federally declared disaster

Occur in a disaster area

Not be compensated by insurance or otherwise

While some taxpayers will fit into this deduction, the rules and procedures are complex.

Examples of deductible losses as a result of COVID-19 vary from costs related to running your business during a pandemic like investments in personal protective equipment and cleaning supplies and services, to the closure of stores and facilities and disposal of unsaleable inventory. Other eligible costs include certain termination payments, losses from property sales or exchanges, abandonment of leasehold improvements, and nonrefundable event payments, to name a few.

To make the Section 165(i) election, taxpayers must include Form 4684, “Casualties and Thefts,” with their return within six months from the due date for filing the taxpayer’s federal income tax return for the disaster year.

We can assist you with identifying your deductible expenses and following the complex rules and procedures for making this election. Reach out for assistance.

With personal income tax representing 61% of California’s total general fund revenue sources, it is no surprise that the California Franchise Tax Board in the last few years has become more aggressive in its enforcement and interpretation of California residency law, using residency audits to do so.

What is California Residency Audit? According to California’s residency laws, residents must pay state tax on their worldwide income, no matter the source of the income. Meanwhile, part-year residents are only required to pay taxes on income received while a resident of the state. Therefore, a person’s “residence” under California law is the key to understanding their state income tax liability. For this reason, the FTB conducts residency audits that will determine a person’s residency.

The 3 Types of “Residency” According to California Residence Law When the FTB conducts a residency audit, the outcomes are generally broken down into three different categories. These are resident, nonresident, or part-year resident. The audit is simply meant to help determine which category taxpayers fall into.

Resident: A taxpayer may be found to be a resident of California, in which case they are taxed on income from all sources, including income from sources outside of California.

Nonresident: A taxpayer may be found to be a nonresident of California, in which case, they are taxed only on income from California sources.

Part-year resident: A taxpayer may be found to be a part-year resident, and taxed on all income received while a resident and only from California sources while a nonresident.

According to California residency is defined as an individual who is in the state for anything else other than a temporary or transitory purpose or domiciled in California but physically outside the state for a temporary or transitory purpose. While the above definition might seem very straightforward, in reality the law is broadly written and leaves room for interpretation. As a result, if the FTB says you are a state resident, the burden now lies with you to prove them wrong.

How the FTB Determines Residency Status California residency law defines the class of persons that are expected to contribute tax revenue to the state. California’s Revenue and Tax Code (R&TC) § 17014 includes every person in the state of California except for those in California for “a temporary or transitory purpose.”

It is important to note that this definition of residency is very broad, and includes everyone currently in the state except for those remaining in the state for a temporary or transitory purpose. It also includes those people domiciled in the state of California but currently outside the state for a temporary or transitory purpose.

Much of the residency determination depends upon the definition of “a temporary or transitory purpose.” California Code of Regulations (CCR) § 17014(b) defines in great detail what “temporary or transitory purpose” means. It states that those domiciled in the state who leave for a short period of time for both business and pleasure are outside the state for “a temporary or transitory purpose,” and as such are to be taxed as California residents.

Those domiciled outside the state, but staying within the state for business, medical or retirement purposes that are long-term and indefinite in time will not be considered in the state for “a temporary or transitory purpose,” and will be subject to the state tax.

As you can see, there is a lot of room for the FTB to interpret your movement as they like. But in general, listed below are the factors that the FTB uses to determine an individual’s residence status:

The amount of time the individual spent in California versus the amount of time spent outside of the state.

The location of the individual’s spouse and children.

The state where the individual’s principal residence is located.

The state that issued the individual’s driver’s license.

The state the individual’s vehicles are registered in.

The state the individual’s professional licenses are maintained in.

The state the individual is registered to vote in.

The location of the individual’s bank accounts.

The origination points of the individual’s financial transactions.

The location of the individual’s medical professionals, as well as accountants and attorneys.

The location of the individual’s social ties such as worship, country clubs and professional associations.

The location of the individual’s real estate property and investments.

The permanence of the individual’s work assignments in California.